[[{“value”:”

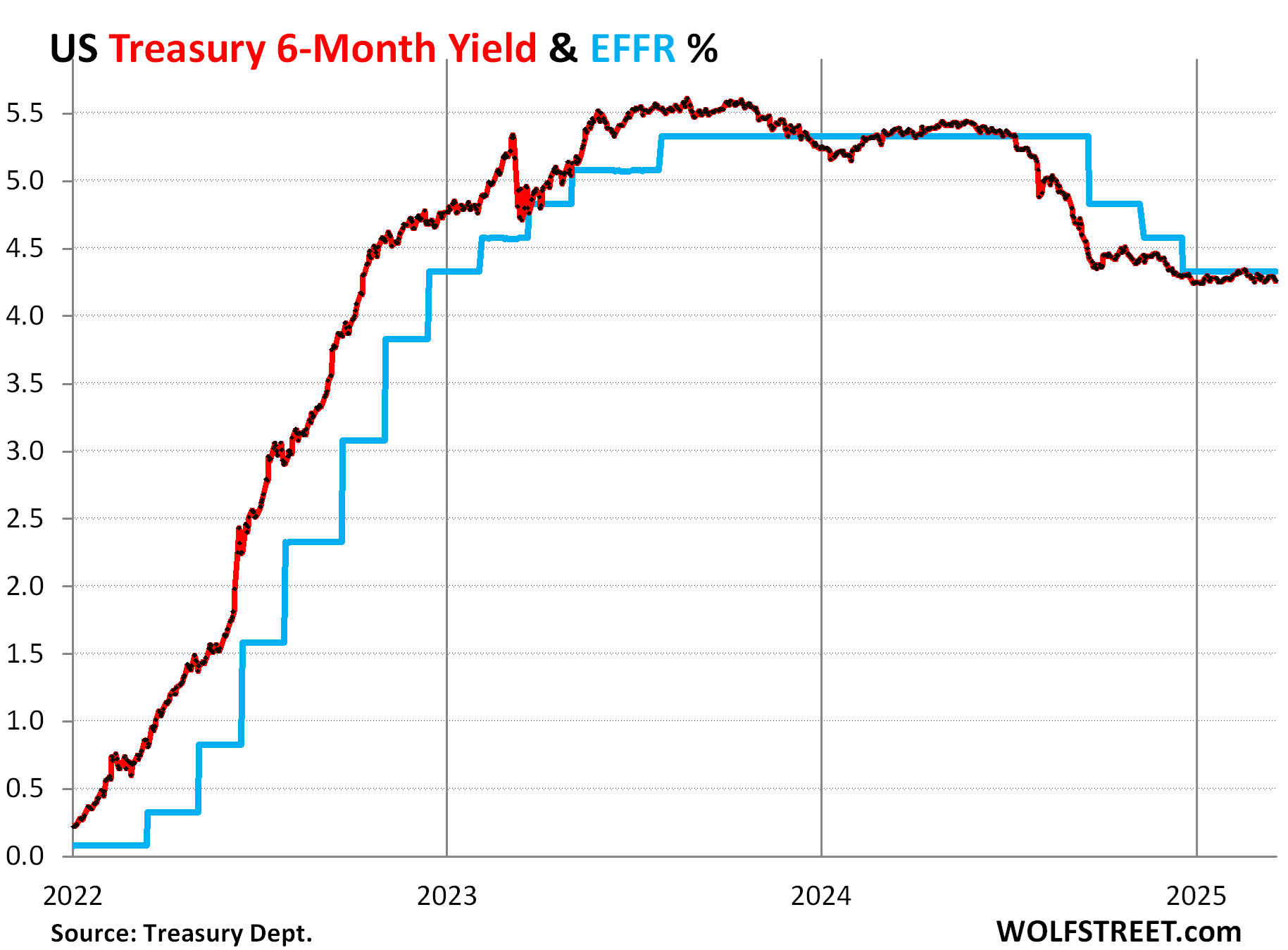

Short-term Treasury yields of 6 months or less stay put above 4%.

By Wolf Richter for WOLF STREET.

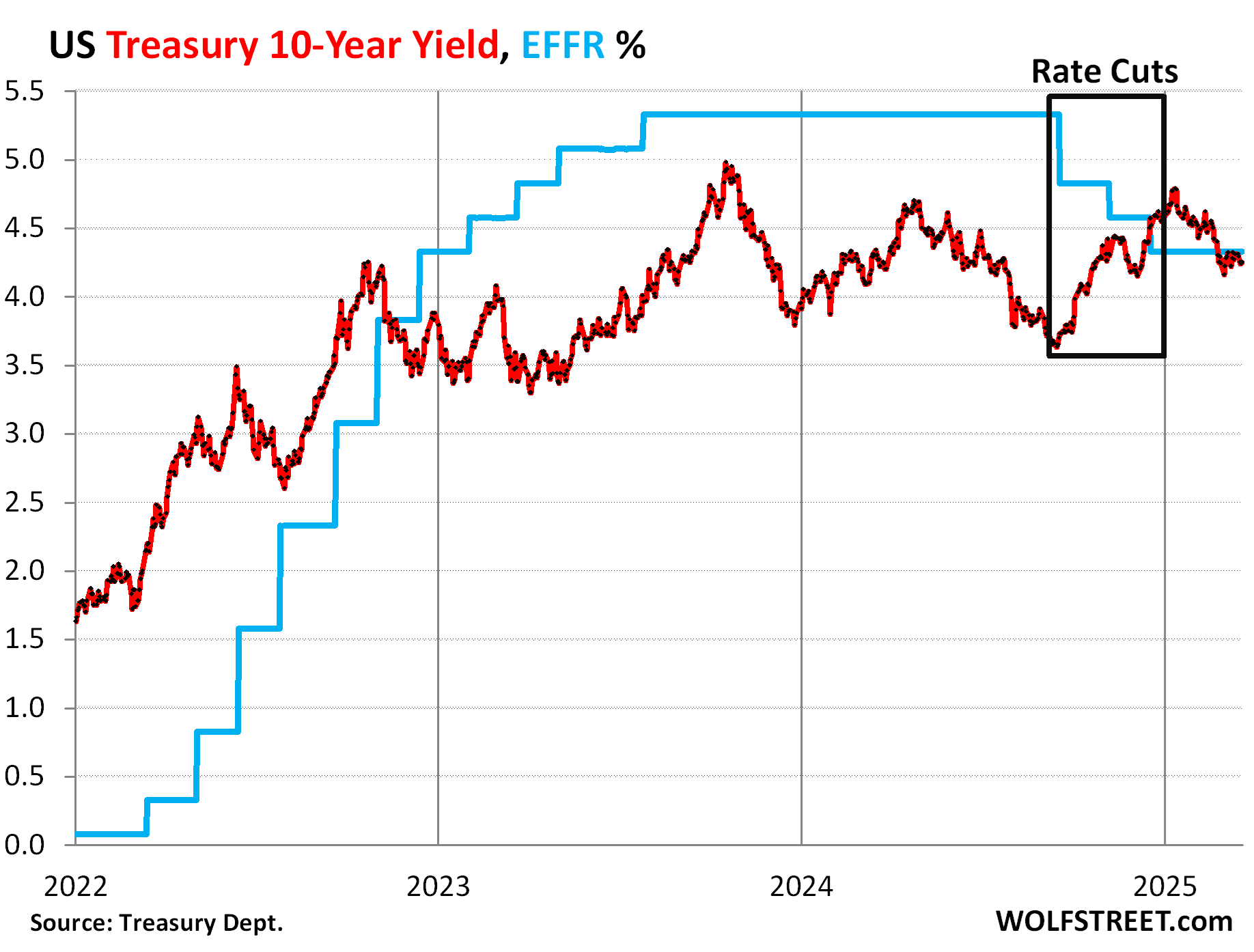

The 10-year Treasury yield has careened lower from 4.77% on January 10 to 4.16% on March 3, and has since then wobbled a little higher to end at 4.26% on Friday, just a hair below the effective federal funds rate (EFFR) that the Fed targets with its short-term policy rates. This decline in the 10-year yield isn’t a coincident.

The government has been trying to push down, talk down, swat down, and wish down long-term Treasury yields to make funding in the economy for businesses and households less costly – the stated policy of Treasury Secretary Scott Bessent.

These efforts have been fortified by the Fed’s more hawkish stance on inflation and interest rates, which put the bond market at ease. The bond market had gotten spooked by the Fed’s 100-basis-points in rate cuts despite re-accelerating inflation, which triggered a bond selloff that had caused the 10-year yield to spike by 114 basis points, even as the Fed cut by 100 basis points. The long-term Treasury market fears out-of-whack inflation more than anything.

That ironic situation when the Fed cut its short-term policy rates by 100 basis points, while the long-term Treasury yields spiked by over 100 basis points, has now been partially unwound.

Despite all the drama and irony of rate cuts accompanies by surging yields, the 10-year Treasury yield has remained in its two-year range and is now in the middle of that range.

We can see the strategy here to get long-term yields down:

- Obviously, the Fed gets more hawkish about inflation and puts rate cuts on ice, after its rate cuts amid accelerating inflation spooked the long-term bond market.

- Treasury reduces supply of long-term securities by shifting issuance to T-bills, which it has been doing for over a year. During the debt ceiling, new supply is on hold anyway.

- Treasury talks down the 10-year yield, which Bessent has been doing.

- The Fed slows the QT of Treasury securities from $25 billion a month to $5 billion, starting in April, though QT of MBS will continue to run at the current rate.

Long-term yields matter to the economy. They’re the base for borrowing costs for businesses and households. While there is some debt with floating rates, the majority of the debt has fixed rates that roughly parallel 10-year Treasury yields, but are higher. A rising 10-year Treasury yield increases borrowing costs for new debt in the economy and tighten financial conditions and eventually slows the economy.

But a lower 10-year yield boosts the economy and might add some fuel to inflation, which would be in line with the Fed’s three-year mantra “higher for longer” – higher Fed policy rates and higher inflation.

But short-term yields of 6 months or less stay put above 4%.

The six-month Treasury yield had already priced in a big part of the 100-basis-points in rate cuts by the time the first rate cut happened, having dropped by 90 basis points from 5.4% in May to 4.5% just before the September cut.

Today, it’s at 4.23%, still glued to the underside of the EFFR, pricing in only a minuscule chance of a rate cut within its window over the next few months.

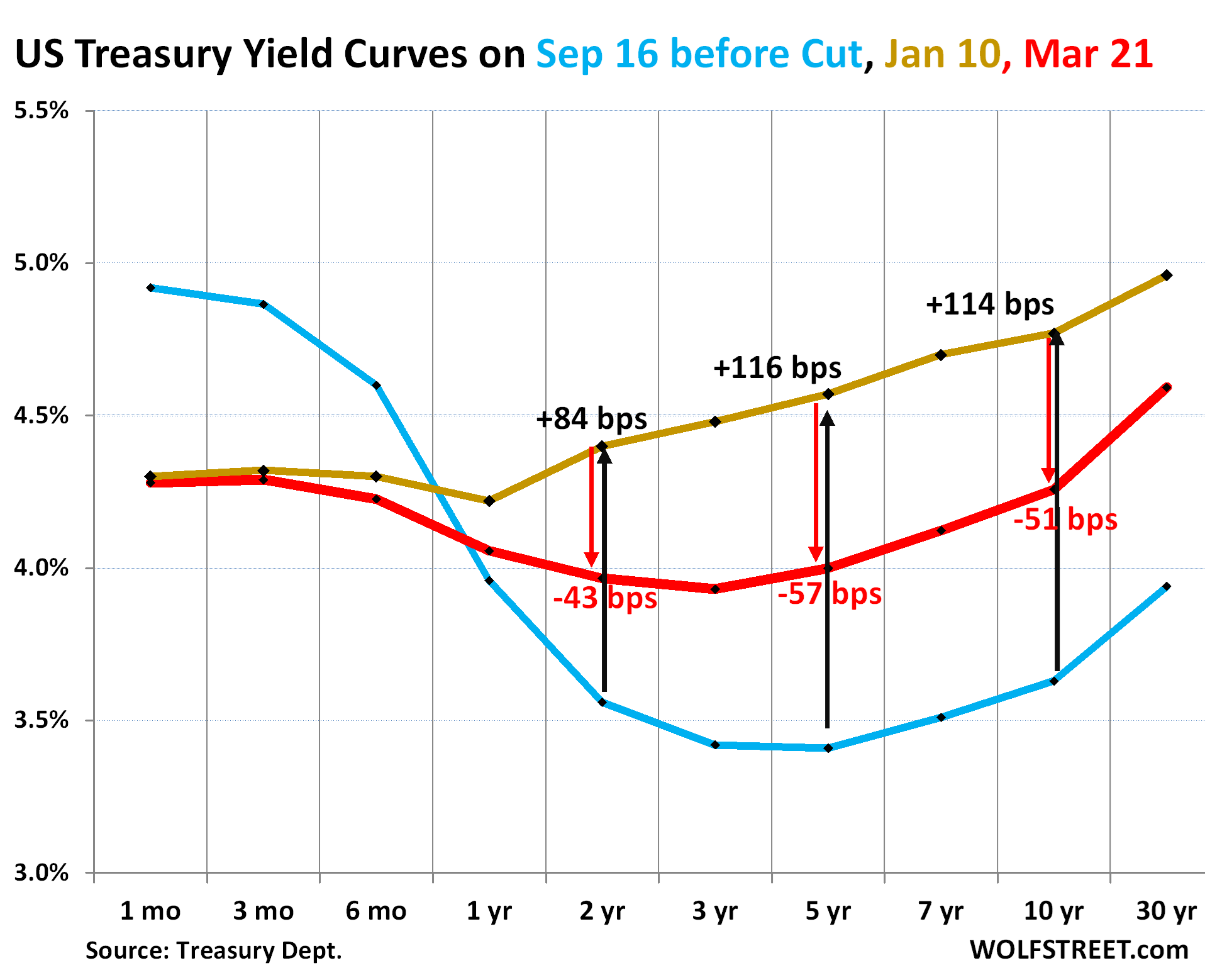

The yield curve has re-inverted with a sag in the middle.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Red: March 21, 2025.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

With rate cuts on ice, short-term yields haven’t budged much and remain glued to the EFFR. But longer-term yields have dropped since January 10. As a result, yields from 1 year through 10 years are now all lower than short-term yields, and only the 20-year yield (4.61%) and the 30-year yield (4.59%) are higher than short-term yields, creating this sag in the middle of the yield curve with the low point at the 3-year yield (red line).

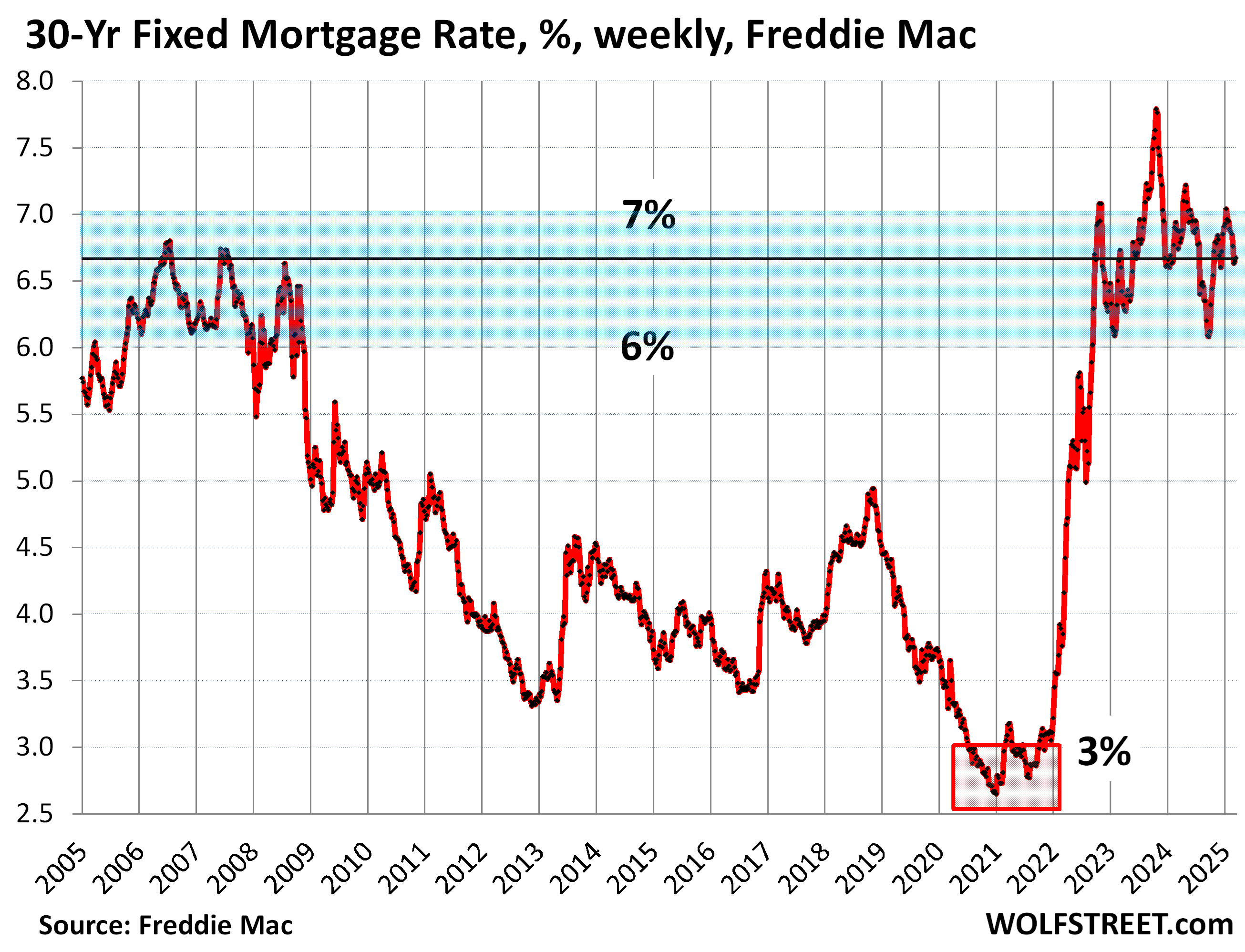

But mortgage rates aren’t fully buying into it.

From mid-September through mid-January, the average 30-year fixed mortgage rate had risen by 96 basis points, to 7.04%, according to Freddie Mac’s weekly measure, while the Fed had cut by 100 basis points, an irony that had perplexed the real estate industry, which had expected the rate cuts to push down mortgage rates.

Mortgage rates have since given up only 37 basis points of this 96-basis point surge – while the 10-year yield gave up 58 basis points, and the spread between the two has widened.

At 6.67%, the average 30-year fixed mortgage rate, per Freddie Mac’s measure, is at the upper half of the 6-7% range that has prevailed since September 2022.

In the three decades between 1972 and 2002, that 7% was the lower edge of the range. For most of that time, rates were above 8%.

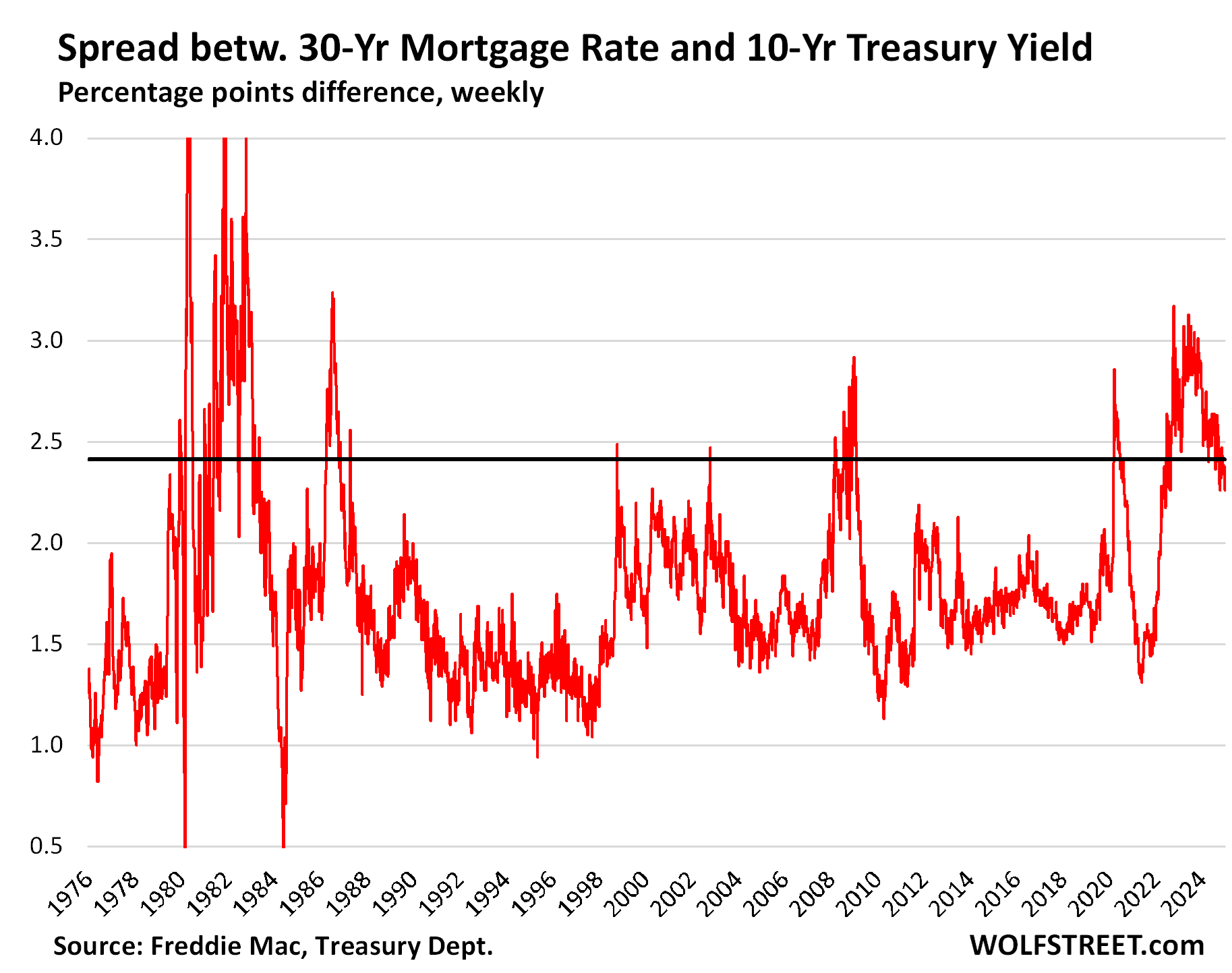

The mortgage-rate spread widened.

The spread between the 30-year mortgage rate and the 10-year Treasury yield widened further, as the 10-year yield fell more than mortgage rates. With the latest move in yields, it widened to 2.41 percentage points.

After QT was announced in the spring of 2022 and kicked off in July 2022, mortgage rates increased faster and further than the 10-year Treasury yield and the spread widened sharply, and eventually exceeded 3 percentage points, which was very wide in historic terms, last seen in 1986. From that high, the spread narrowed to 2.41 percentage points now, but remains very wide historically.:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Treasury Yield Curve Re-Inverts with Sag in the Middle, as Government Swats Down 10-Year Yield. But Mortgage Rates Don’t Follow all the Way, Spread Widens appeared first on Energy News Beat.

“}]]

Energy News Beat