[[{“value”:”

Long-term yields matter more to the economy than the Fed’s short-term policy rates; hence the efforts to push them down.

By Wolf Richter for WOLF STREET.

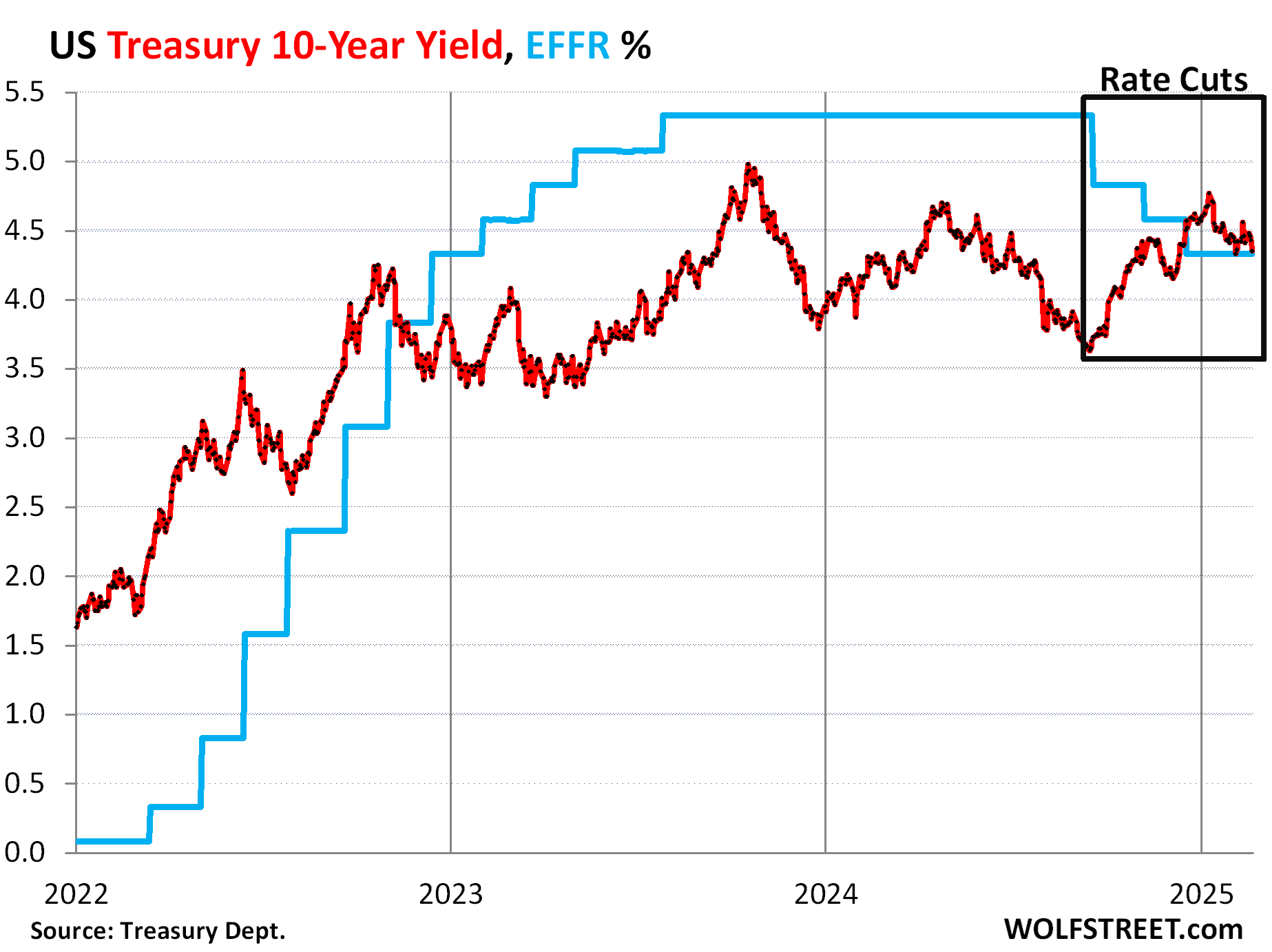

The 10-year Treasury yield dropped by 8 basis points on Friday, to 4.43%, perhaps inspired by iffy feelings elsewhere as stocks careened lower and investors sought safety.

Since January 10, the 10-year yield has now given up 34 basis points of that 114-basis-point spike that it had experienced from mid-September 2024, just before the Fed’s first cut, through January 10, 2025. Over this period of surging long-term yields, the Fed had cut its short-term policy rates by 100 basis points.

The Effective Federal Funds Rate (EFFR), which the Fed targets with its policy rates, has remained at 4.33% since the December rate cut, down by 100 basis points from the pre-cut levels (blue).

One of the reasons for this massive disconnect was the market’s assumption that the Fed, amid its rate cuts and rate-cut talk, would be lax about inflation, which just at the nick of time had started to re-accelerate. And further rate cuts could provide additional fuel for it. Rising inflation and a lax Fed spook the long-term fixed-income market.

Long-term yields really matter to the economy. They reflect the borrowing costs for businesses and households. There is some debt with floating rates, but the majority of the debt has fixed rates that track 10-year Treasury yields, and higher 10-year yields would increase actual borrowing costs for new debt in the economy and tighten financial conditions and eventually slow the economy.

These rate cuts, and the formerly-projected future rate cuts, in light of the inflation scenario developing over the past few months, had the effect of spooking investors who wanted to be compensated more for those higher inflation risks over those 10 years, which pushed up long-term yields.

So how to you get the 10-year yield to go down?

Not with rate cuts, obviously. That flopped and had the opposite effect. But with a three-pronged strategy:

- The Fed gets more hawkish about inflation and puts further rate cuts on ice.

- The Treasury Department minimizes the supply of long-term Treasury securities, by shifting issuance to short-term securities, which it has been doing for over a year; and by deficit reduction, which is new.

- The Fed and Treasury Department both talk down the 10-year Treasury yield.

So the Fed got more concerned about inflation at the December meeting, when it cut one more time, but projected only two cuts in 2025, and saw higher inflation and higher “longer run” rates. At the January meeting when it didn’t cut, the Fed pivoted to wait-and-see and put further cuts on ice.

Then on February 6, Treasury Secretary Scott Bessent came out and said in an interview that “The president wants lower rates,” but that “he and I are focused on the 10-year Treasury and what is the yield of that.”

So lower long-term rates. And how do you get long-term rates down? Get inflation down and keep it down. And that’s the Fed’s job. And rate cuts won’t do that job. The Fed cannot be lax about inflation, that became abundantly clear, because a lax Fed in an inflationary environment would drive up long-term yields.

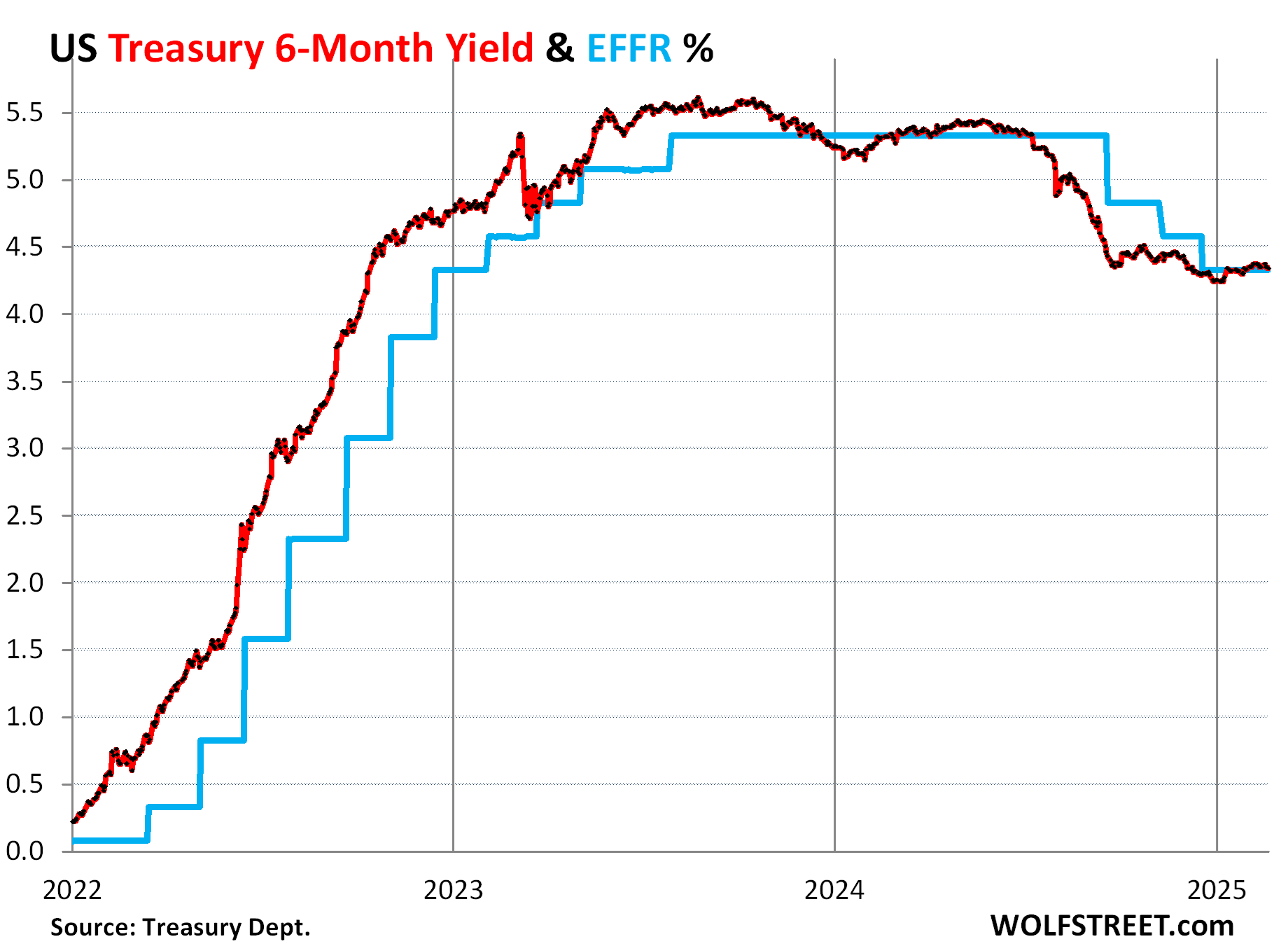

Short-term yields stayed put.

Short-term yields essentially haven’t budged since early December when they had already fully priced in the rate cut at the time.

The six-month yield no longer prices in any rate cuts in its window through mid-2025 before it matures, hovering right around the EFFR.

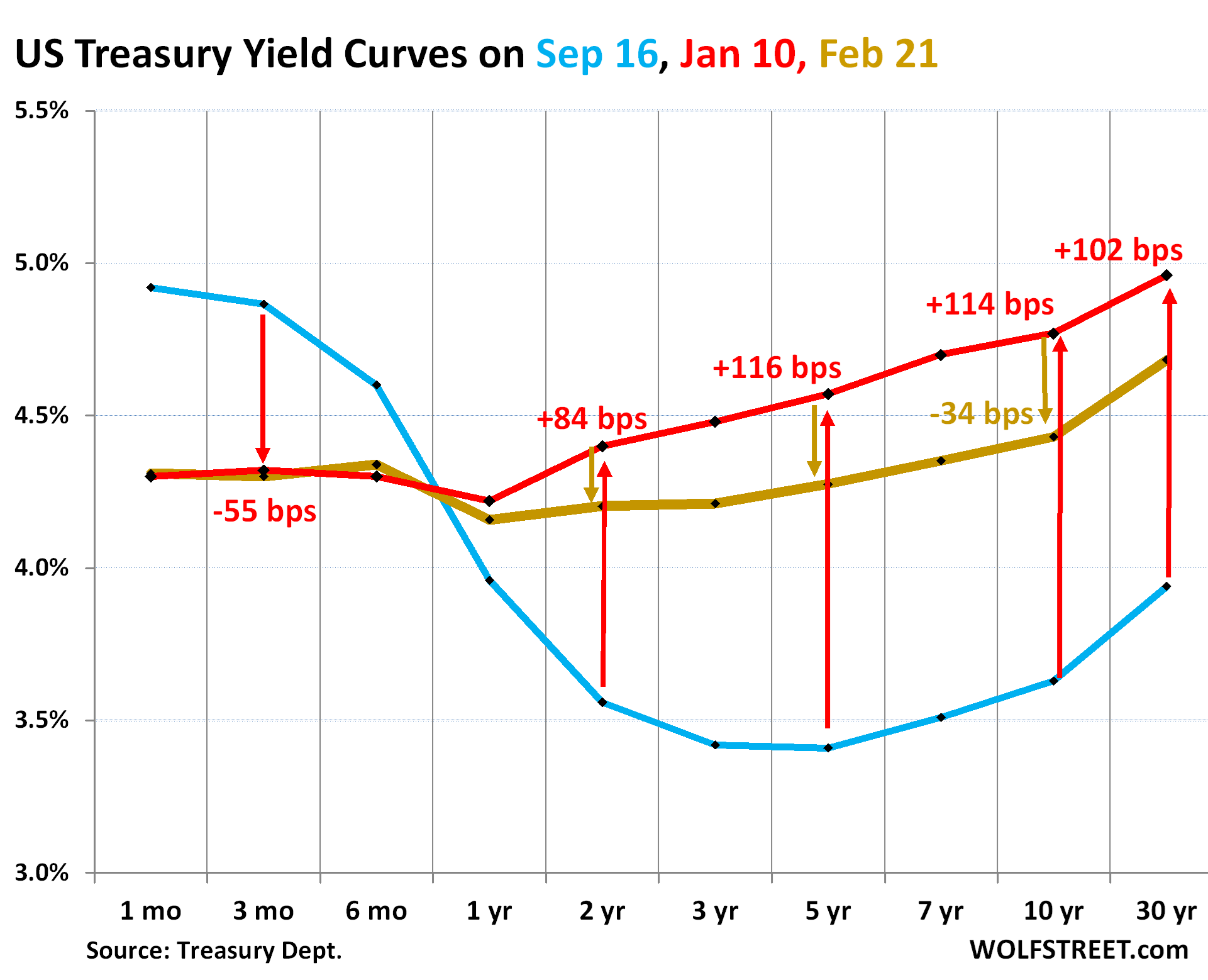

The yield curve flattened.

With the Fed having put rate cuts on ice, short-term yields stayed put at around the EFFR, while long-term yields came down some. As a result, the yield curve flattened some.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: January 10, 2025, just before the Fed pivoted to wait-and-see.

- Gold: Friday, February 21, 2025.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

This yield curve has a dip at the one-year yield, with the 6-month yield being higher than yields in the range of 1-5 years.

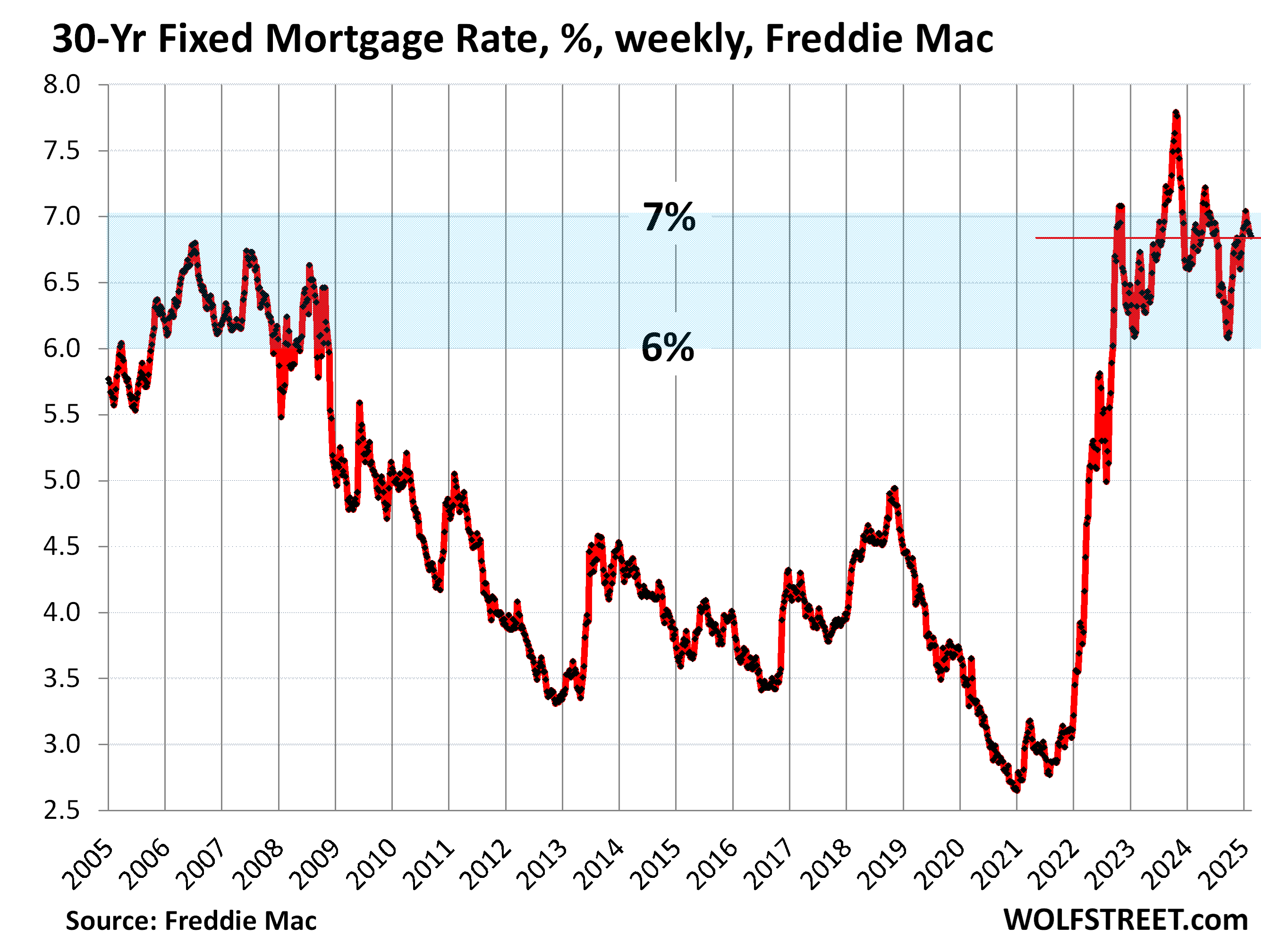

But mortgage rates remain close to 7%.

From the initial rate cut in September through mid-January, just before the Fed pivoted to wait-and-see, the average 30-year fixed mortgage rate had risen by 96 basis points, to 7.04%, according to Freddie Mac’s weekly measure, while the Fed had cut by 100 basis points.

Mortgage rates have since given up only 19 basis points of this 96-basis point surge, and at 6.85% are at the upper end of the 6-7% range in which they have been since September 2022.

Over the three decades between 1972 and 2002, 7% was the lower edge of the range, and for most of that time, rates were above 8%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Treasury Yield Curve Flattens as 10-Year Yield Falls, Short-Term Yields Stay Put: Fed’s Pivot to Wait-and-See in Inflationary Times. But Mortgage Rates Stay Near 7% appeared first on Energy News Beat.

“}]]

Energy News Beat