Marathon Oil Corporation has a sound balance sheet that has been very free with returning capital to shareholders with both dividends and buybacks.

We won’t be rid of oil and gas for many more decades, and in the meantime, staying invested in companies like Marathon can prove to generate good returns.

I will rate Marathon a buy because of the quality of the business and the solid management team.

Investment Rundown

Marathon Oil Corporation (NYSE:MRO) is a United States-based company that focuses on discovering, extracting, and refining oil and natural gas resources. The company operates in various locations across North America, Africa, and the Middle East. Marathon Oil Corporation is dedicated to utilizing advanced technology and innovative techniques to maximize the production of oil and gas while minimizing environmental impact. They continue making strategic investments and acquisitions to help bolster their market share and solidify shareholder value for the coming years. The acquisition of Eagle Ford assets in Ensign Natural Resources gives the company immediate cash flows but still the potential for growth and future development. Moves like these help the company achieve a ROC of above 12%.

{kind=link}

Company Highlights (Investor Presentation)

A global presence has helped the company be able to achieve strong revenues and the company showcased in the last earnings report they are able to ride the wave even more and deliver a lot of value to shareholders. The announcement of another dividend is easy when the company is able to generate over $7 billion in TTM revenues and keep an FCF above 30%. I think there will be a green transition in our society eventually, but the need for both oil and gas is still too large to make the case the companies aren’t worth investing in. I think Marathon is an incredibly solid company and I would be happy to be invested in them.

Green Transition Won’t Stop Demand For MRO

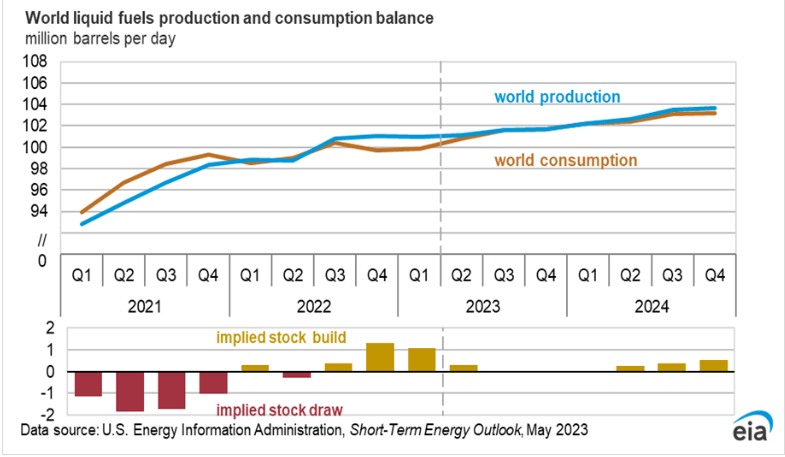

As I mentioned earlier, it’s unlikely that we will completely move away from oil and natural gas in the near future, as there are several major trends that need to shift first. India’s emerging market may provide a new source of demand for these resources, even if demand in the US slows down. While Marathon may not necessarily set up projects in India, there will likely be continued global demand that keeps the company in business, as its services remain in use. In the US, natural gas doesn’t seem to be slowing down either, with a projected 3% increase from 2022 levels expected in 2023. This contradicts the notion that we are moving towards a greener society.

{kind=link}

Oil Estimates (IEA)

To capitalize on this trend Marathon is pushing a lot of capital to shareholders through both dividends and buybacks. The environment is shaky but estimates are that oil will recover even if sentiments remain negative as people want to rid themselves of the need for nonrenewable energy sources.

{kind=link}

Company Strategy (Investor Presentation)

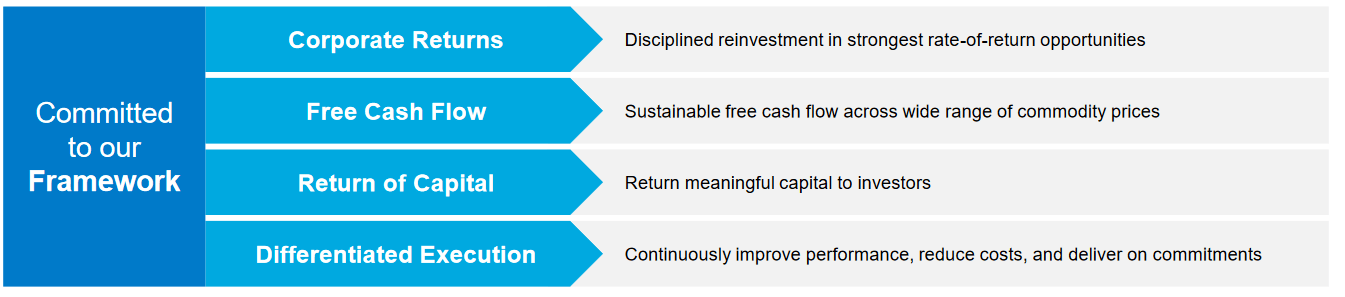

What Marathon is doing is trying to get ahead of the trend that eventually we won’t need oil and gas in our societies. But as mentioned, that is far, far away and in the meantime, there is ample opportunity for investors to gain from the profits these companies are doing. With accusations and the priority of keeping a clean and efficient balance sheet, Marathon is in a strong position to grow from any tailwinds appearing in the industry.

Latest Earnings Call

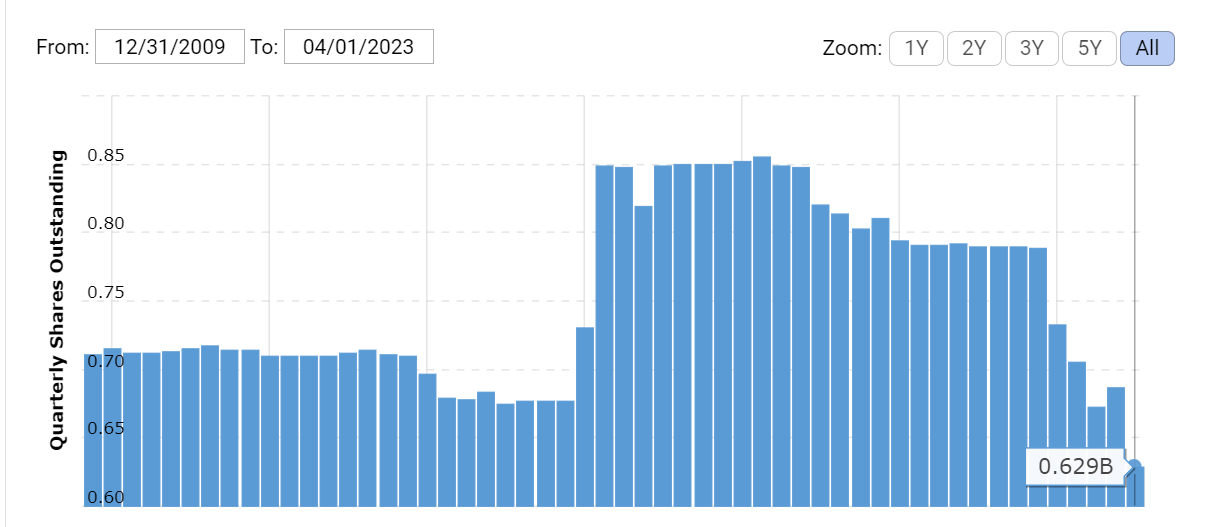

In the last earnings report from the company it was clear Marathon had another strong quarter of growth and return of capital to investors. They have done so with both dividends and buybacks. In the quarter that would be $397 million whereas $334 million was used for buybacks.

{kind=link}

Shares Outstanding (Macrotrends)

What I like about this move especially is that Marathon isn’t buying when the valuation is high, the forward p/e might be rising but it still sits at just around 8, which is in line with the sector. I think this showcases the company isn’t necessarily overpaying with these buybacks. Since the inception of Marathon’s large share buybacks program back in 2021, the company has decreased the outstanding amount by around 22%. Investors have gained tremendously from this move as the share price has also tripled since that time.

In the report, the CEO Lee Tillman also said the following about the quarter, “With $2 billion of outstanding share repurchase authorization, we expect to continue buying back our stock to drive peer-leading growth in per-share metrics. We further strengthened our portfolio by successfully integrating the highly accretive Ensign Natural Resources asset ahead of schedule and signed an HOA to develop future phases of the E.G. Gas Mega Hub”. To touch on this further, I think the strategy of buying back shares to drive EPS growth is a sound move given that the cash flows generated are so vast in the industry and this is often the best move forward. Fluctuations in oil prices will continue to happen, but Marathon is showcasing they have been able to keep margins high despite this.

Risks

The major risk for companies exposed to oil and natural gas is that the prices remain soft or low. Often caused by the fears of recessions, but as we have seen in recent months, that fear seems to continuously be prolonged as we haven’t quite yet hit some of the marks to qualify for it.

If a recession was to hit and we would see significantly lower commodity prices I do expect the share price of Marathon to fall with it.

Perhaps not a risk, but instead a wish for Marathon is that they place a higher priority on increasing the cash position they have currently. It’s not even above $200 million, of course, affected tb the acquisition of Eagle Ford assets in Ensign Natural Resources where the deal landed at $3 billion. When the company is generating above $2 billion in levered free cash flows in the last 12 months I think it would be wise to build this position back up again to help against other times when oil prices might be suppressed and margins lower. It would benefit investors as a dividend could still be distributed.

Valuation and Article Summary

Right now it seems that Marathon is in line with the sector in terms of a p/e valuation as the forward numbers sit around 8. But where Marathon wins out is both the p/fcf and EV/EBITDA.

{kind=link}

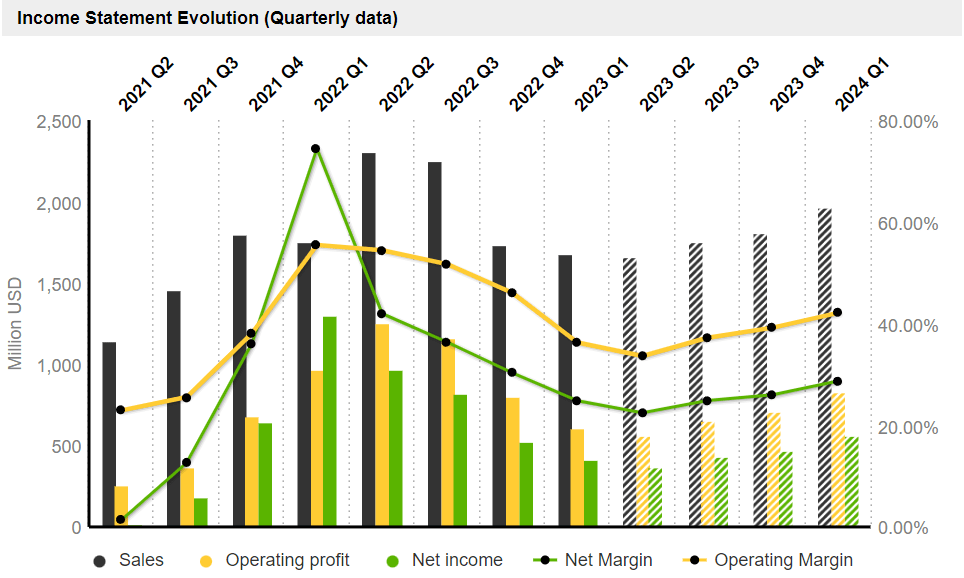

Company Income Statement (Investor Presentation)

The results seen in the last 2 years I don’t think are sustainable, and that seems to be the consensus for most people. So right now, investing in Marathon would be because you want exposure to the industry when the next boom comes along. Until then I think it’s incredibly important to place capital in a company that has sound financials and priorities giving back to shareholders even during tough times. Here Marathon seems to tick every box. A margin decrease in 2023 seems fair, but a return upwards is very plausible as many analysts see a return toward $100 per barrel in April 2024 as said in a report by Reuters. I don’t see Marathon as necessarily a strong buy right now, the valuation is like I said in line with the sector, but it doesn’t constitute a hold either as the future seems to promise to miss out on some of the appreciation possible. The share price seems to be in a downward trend and I see any large drop as a good opportunity to add more to a position.

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack

The post Marathon Oil Keeps Growing And Providing Long-Term Value appeared first on Energy News Beat.

Energy News Beat