Authored by Jeffrey Snider via RealClearMarkets.com,

It was a sudden and epic flood of oil the likes of which the country hadn’t seen before. According to the government’s numbers, the Energy Information Administration, over a seven-week period domestic stocks of crude gushed by a then-record 34.4 million barrels. The last time America had experienced close to that number was March and April 1990, just prior to the start of what should have been called the S&L recession.

{kind=link}

This was again March and April, though in the year 2001. Up to the prior November, policymakers and Economists had refused to consider anything other than inflation as their top priority, much of it – as always – driven by oil prices.

WTI, the major US benchmark, had been under $20 per barrel in the summer of 1999. From then, prices started to rise and by the time the NASDAQ would reach its epic top in early 2000 crude was trading just more than $34. Consumer price indices reflected that jump.

It would slack off over the following months before a late summer rebound rekindled Alan Greenspan’s (faulty) inflation instincts. Back at $37 a barrel in September 2000, even as clear signs of economic weakness spread throughout the macro catalog, the “maestro” was far more concerned about the tight labor market he and his colleagues perceived.

That’s the funny thing about CPIs and PCE Deflators, or one of the weirdest aspects of how they’re used. Variation in those is most directly attributable to WTI and its influence on gasoline. There is, and remains today, a steady and dependable correlation.

Yet, for all the fuss and bother over perceived inflation risks, at the FOMC, anyway, it never has much to do with oil, how oil gets used and by how much. Rather, policymakers place all their focus on the bastardization of the relationship British economist AW Phillips once upon a time had modestly suggested.

The Phillips Curve proposes a link between tight labor markets, as denoted by a very low unemployment rate, and competition for workers. Scarcity among them in a robust economy would lead firms to increase wage and pay scales as fewer become readily available, raising input costs which those businesses might rationally pass along to their consumer customers in what’s (incorrectly) called inflation.

Should the labor market be so good, consumers as workers would be able to afford higher prices, absorbing them but not before demanding even higher pay back on the job; the dreaded and totally theoretical wage-price spiral.

As late as November 2000, the FOMC would not budge from the unemployment rate.

“CHAIRMAN GREENSPAN. All in all, I think that we have, as all of you have said, a combination of the potential persistence of significant inflationary pressures and an unquestioned increase in overall signs of weakness. In other words, my judgment, and I guess I agree with almost everybody else, is that it would be premature to move to a balanced risk statement.”

Up to that time, policymakers at least had oil prices on their side, so to speak. WTI would bounce around in the $30s from September forward, and by the time the Committee met in November it was still up around $35. As a result, consumer price indices would likewise remain uncomfortable considering the Fed’s implicit inflation targeting somewhere around 2%.

Sure enough, from the moment Chairman Greenspan uttered those words, oil would tumble. By the end of 2000, it would reach the $25s just as the FOMC completely reversed course and began cutting its federal funds target once 2001 began.

They did so not yet convinced the US was experiencing any worse than a minor slowdown. The purpose of the initial rate cut as well as the few more which quickly followed was to ensure exactly that, the economy would decelerate but not fall into a recession; to engineer what some would call a soft landing.

The idea, even expectation of one persisted despite more troubling developments, including the sudden surge of oil inventories which from the outside had been a clear sign – like Spring 1990 – that something was badly amiss in terms of general economic demand.

Another such warning came on April 18, 2001. On that date, the FOMC was hastily gathered telephonically to rubber stamp the third consecutive 50-bps rate cut, this one unscheduled. While the group was talking, the Census Bureau reported US trade figures for the month of March.

The country’s merchandise deficit fell sharply because, in the words of Greenspan that day, “In short, they show a significant decline in imports. In fact, I think it is the sharpest decline we’ve had in many years.” While a few policymakers thought this some kind of positive, notably Vice Chairman Bill McDonough (who actually said, out loud, the following: “The drop in merchandise imports is good news for our economy”), any rational thinkers among the bunch knew it indicated nothing of the sort.

Along with the sharp rise in oil inventories, the equally sharp fall in imports signaled the start of what only later would be dated and called the dot-com recession.

Before the NBER would finally make their call much later on November 26, only then noting how March 2001 must have been when it began, for some time further forecasts still called for the same soft landing. In the middle of May, for example, Economist Dave Stockton presented the staff’s projections which even then showed, “First, we believe that the economy, at present, is very weak–not in recession, but not far from it either.”

The primary reason for that weakness was, back to Mr. Stockton, “the most intense weakness remains centered in the factory sector.” Inventories of all goods and not just oil had jumped as consumer and business demand had declined if only modestly, thus accounting for imports, that oil glut, the entirety of what became the dot-com contraction.

Over the two decades-plus since then, hardly anything has changed how the economy works or how the Fed thinks about it. Inflation bias remains as strong as ever (2021 aside), and the vast majority of it continues to be drawn from the Phillips Curve perspective. Yet, like before, the CPI will be most affected by what does happen from oil.

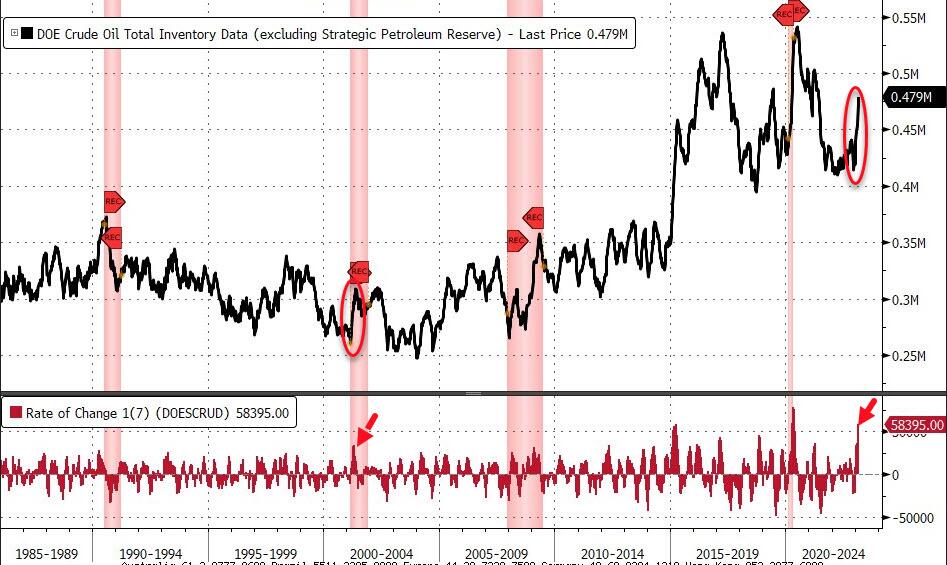

According to the EIA’s latest estimates right up to last week, oil inventories in the US have absolutely exploded, rising an incredible 58.4 million barrels in just seven weeks (the same period of comparison as stated earlier for 2001). This is, obviously, nearly double the glut from twenty-two winters ago.

{kind=link}

While not a new record, this fact provides very little comfort. The only seven-week period when crude stocks rose more was that time when COVID fears had shut down large swaths of economic, civil, and just daily life in the country – from the week of March 13 to and including the week of May 1, 2020, domestic inventories added 78.5 million barrels.

To be even in the same general vicinity as then is a huge warning.

The only other instance when oil inventories have gained as much in such a short period was February and March 2015. Back then, the massive rise was immediately blamed on shale oil production as if output which had taken years of investment to pull off had been surprisingly robust all of a sudden.

While supplies did indeed grow, that growth has hardly unanticipated. What had been, as always, was a sharp drop in global and domestic demand, the former in the form of a major depression in economies worldwide, devastating particularly emerging markets beginning with China and in a way none of them have yet recovered.

That in mind, it was China especially upon which many had pinned their hopes for 2023 revival. Rationalizing Xi Jinping’s highly irrational (from a certain view) Zero-COVID as the reason for the Chinese stumbling in 2022, its removal at the end of last year was spun into the greatest relief effort just in the nick of time.

Despite so much radical hype, it isn’t showing up in these places where it really should. As the world’s largest user and importer of oil, an unfettered and legitimately rebounding China economy would have scavenged every last drop of spare oil from the world’s hamstrung crude producers.

Rather than surge, domestic stocks would be drained even more than they had been last year as the thirsty crude dragon reawakened to its high energy needs.

But this isn’t just about the (inevitable?) thorough disappointment about to flood the world from that side of the Pacific. It is, like 2001 and 1990, quite a lot about US demand, too. Furthermore, it should be pointed out the US imports of goods were down huge last November (before very modestly rebounding in December; January figures have yet to be released).

The oil market has been pricing therefore predicting this scenario from way back when US inbound trade was crashing to finish up 2022. Domestic crude futures had shifted into small but noticeable and more importantly persisting contango since the middle part of November.

This particular shape induces more crude oil toward storage than to be used immediately, a financial incentive where future months’ prices are higher than the current contract rewarding anyone to buy oil on the spot market today to store until those future months having already sold it forward at the higher futures price.

In a situation where supply is as low and perpetually limited as the entire global system has been experiencing since 2020, any modest contango should not be happening. Rewarding the taking of current supply off the market for storage when oil supply has been the single biggest factor behind the world’s “inflation” problem, this just goes to show how much demand must’ve changed.

For those currently occupying those cushy seats at the FOMC, like 2001 this solves their “inflation dilemma” since the oil prices which actually do drive consumer price indices aren’t likely at all to do much more menacing. But what that really means is how this unfortunately opens up the very serious possibility recession has already happened.

What’s mainly in question today is how long before anyone captured by Greenspan lore realizes it. From the last FOMC meeting minutes released this week, as always officials continue to be wholly concentrated on the “tight” labor market as many see it and what the Phillips theory tells them to expect for subsequent consumer price pressures that are already being set instead by this abrupt glut of oil.

Once they do realize, as inverted curves have been long predicting, what follows will be the usual conference calls and emergency rate cuts.

Then many months further down the road the NBER will come along to confirm what by then will have been obvious to everyone unattached to the mainstream Economics discipline.

There are always those who say this time is different when it comes to curve inversions, for a variety of often disingenuous and occasionally comical “reasons.” This time has been no different in that regard. It’s also near exactly the same in a whole bunch of other ways, too, starting with the Fed’s fixation on misleading labor data, then its unnatural need to disregard the oil market for at least making useful forecasts about the CPI.

Consumer prices aren’t the problem, not anymore. Right when optimism and even talk of “transitory disinflation” have been heating up, suddenly all the oil in the world has shown up to spoil those and a whole lot more.

Loading…

The post Is The Recession Already Here? appeared first on Energy News Beat.

Energy News Beat