ESG scoring and mandates remain a subject we have contested since it sprang to life in 2020. The push of “woke activism” on, and by companies, to meet nebulous or artificial standards has led to various bad outcomes.

ESG refers to the Environmental, Social, and Governance risk theoretically embedded in a business. However, while ESG investing is about taking these risks into account in investment decisions, these are all the things NOT on a company’s balance sheet or earnings statements. Such is the inherent problem.

However, as is also the case, with the recent surge in liberal policies, woke activism, and demand for social justice, Wall Street is more than willing to sell products to fill a need. Not surprisingly, with plenty of media coverage, ESG investing became an enormous business.

Following the financial crisis, ESG funds had roughly a ZERO market share of total assets under management. In 2020, ESG-labelled funds in the United States exceeded $16 trillion. It was projected that these funds would exceed $50 trillion by 2025. However, the U.S., which accounts for 11 percent of ESG fund assets, saw outflows of $6.2 billion during the final quarter of 2022.

What caused these outflows from ESG? The answer is not surprising.

“To begin with, ESG funds certainly perform poorly in financial terms. In a recent Journal of Finance paper, University of Chicago researchers analyzed the Morningstar sustainability ratings of more than 20,000 mutual funds representing over $8 trillion of investor savings. Although the highest rated funds in terms of sustainability certainly attracted more capital than the lowest rated funds, none of the high sustainability funds outperformed any of the lowest rated funds.

That result might be expected, and it is possible that investors would be happy to sacrifice financial returns in exchange for better ESG performance. Unfortunately ESG funds don’t seem to deliver better ESG performance either.” – Harvard Business Review

Dying Its Inevitable Death

In our previous discussions of ESG, we warned that the entire premise was highly flawed. I have provided the links below to those commentaries:

ESG Investing – The Great Wall Street Money Heist

Wall Street Wins Again As ESG Scam Infiltrates Retirement Plans

ESG Underperformance Will Be Its Undoing

However, performance, was always going to the reason why ESG failed. The reason we know this is that we have seen these investment schemes before. In the late ’90s, Wall Street moved to limit investing in “sin” stocks such as gambling, tobacco, etc. Just as it was then, investors initially jumped on board, but when returns failed to outperform the benchmark index, that “fad” died.

The same occured in 2021 as investors who wanted to “feel good” about owning “disruptive” companies. That speculative demand changed quickly when performance failed.

{kind=link}

RBC Wealth Management surveyed over 900 US-based clients recently. 49% said that performance and returns were a higher priority than ESG impact, up from 42% in 2021.

“The story told is you don’t have to give up returns in order to do ESG. But everyone assumed that you would get the same exact return profile as a traditional benchmark. Which is absolutely not true because traditional benchmarks are not looking at ESG factors.” – Kent McClanahan, VP Responsible Investing at RBC.

RBC clients also expressed skepticism about the ESG label. 74% of those surveyed said many companies provide misleading information about their ESG initiatives.

“Investment managers and banks are taking advantage of our collective willingness to help fight climate change because the ESG space is, to put it mildly, a zoo.

Epic greenwashing is everywhere: Out of 253 funds that switched to an ESG focus in 2020 in the US, 87 percent of them rebranded by adding words such as ‘sustainable’ or “ESG” or ‘green’ or ‘climate’ to their names.

None changed their stock or bond holdings at that point.” – The Great Wall Street Heist

Unfortunately, changing your name doesn’t change your performance. As RBC noted, performance is all that ultimately matters to investors.

However, ESG was a profoundly flawed premise in the first place.

Deeply Flawed Premise

One of the most significant problems with ESG is that by applying un-measurable factors on companies, such inevitably leads to poor decisions. Environment or social issues may sound great as a talking point but delivering on those goals can be extremely costly.

“Why are ESG funds doing so badly? Part of the explanation may simply be that an express focus on ESG is redundant: in competitive labor markets and product markets, corporate managers trying to maximize long-term shareholder value should of their own accord pay attention to employee, customer, community, and environmental interests. On this basis, setting ESG targets may actually distort decision making.

There’s also some evidence that companies publicly embrace ESG as a cover for poor business performance. A recent paper by Ryan Flugum of the University of Northern Iowa and Matthew Souther of the University of South Carolina reported that when managers underperformed the earnings expectations (set by analysts following their company), they often publicly talked about their focus on ESG. But when they exceeded earnings expectations, they made few, if any, public statements related to ESG. Hence, sustainable fund managers who direct their investments to companies publicly embracing ESG principles may be over-investing in financially underperforming companies.” – Harvard Business Review

In other words, companies will focus on the issues that make them most productive in a competitive, capitalistic environment. However, when companies are forced to make decisions based on meeting some phantom goal or agenda, those choices may not be in the company’s best interest. We have seen recent evidence of blowback from these choices in companies like Anheuser-Busch, Target, and others.

However, while these individual companies have faced backlash by offending large portions of their customer base, it is potentially not entirely their fault.

Blackrock manages over $10 Trillion in assets and has infiltrated itself just about every corner of the financial realm. Given their massive financial presence, they have large stakes in these companies pushing Blackrock’s ESG agenda. The question is, why would they do that? Larry Fink, the CEO of Blackrock, can answer that best.

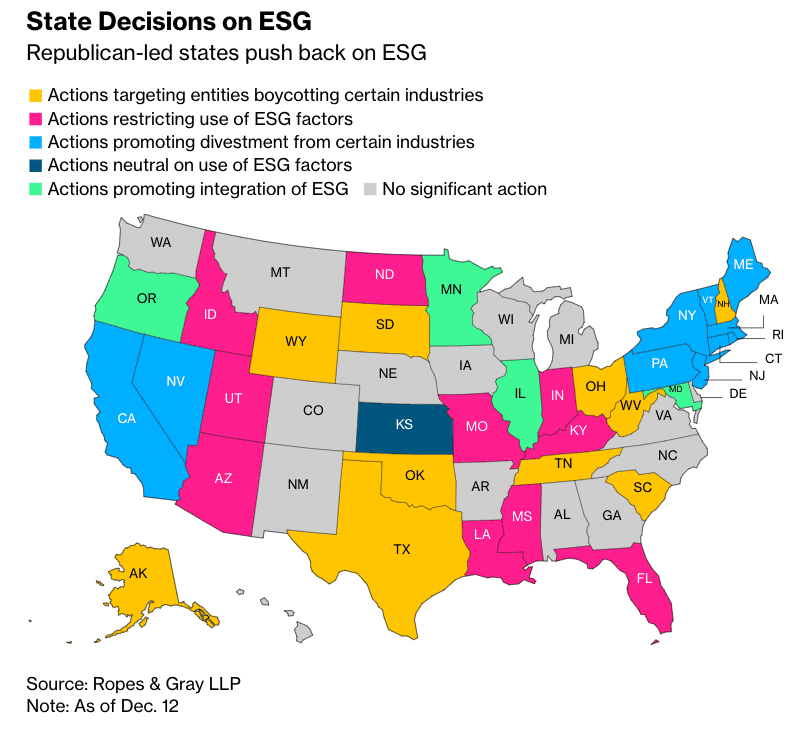

Of course, not only are investors figuring it out, but so are state pension funds.

“Lawmakers from red states have called out BlackRock for its toxic woke capitalism push in corporate America. Besides Florida, states like Louisiana, South Carolina, Utah, Arkansas, West Virginia, Missouri, and Texas have withdrawn funds from the asset manager.”

{kind=link}

While consumers have certainly punished companies that overstepped boundaries on ESG issues recently, maybe the company we should boycott is Blackrock itself. A concerted effort to either pull funds or choosing not to invest in its products may send the most explicit message that the real focus should be on fundamental performance first and foremost.

Since investors vote with their dollars, such mainly explains why ESG is dying its inevitable death.

Source: Realinvestmentadvice.com

by Lance Roberts

The post ESG Is Dying Its Inevitable Death – But will it open up capital for energy investments? appeared first on Energy News Beat.

Energy News Beat