[[{“value”:”

By Wolf Richter for WOLF STREET.

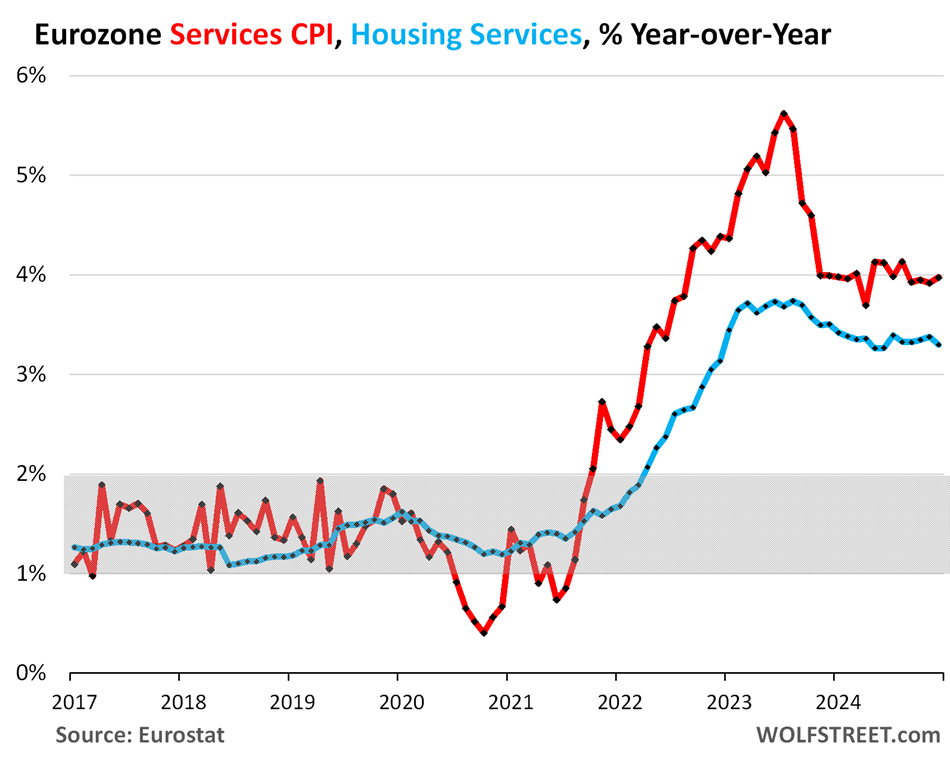

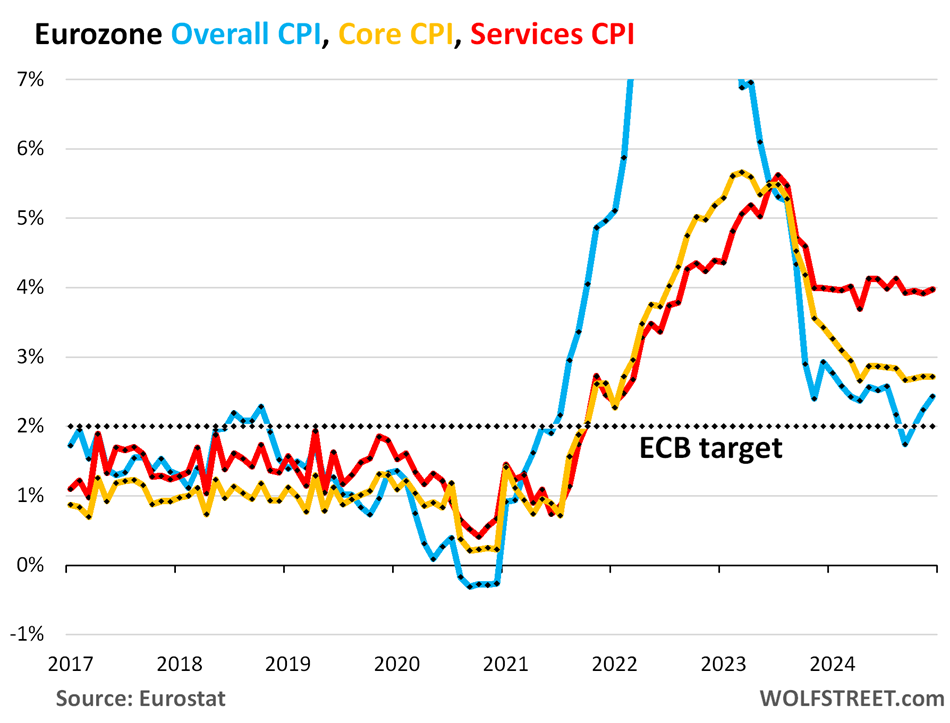

Services inflation in the 20 countries that use the euro accelerated to +4.0% in December, according to Eurostat today. This marks the 13th month in a row that the services CPI has been in the 4.0% range, roughly two to four times what prevailed before the pandemic (between +1% and +2%), and two full percentage points above the peaks before the pandemic and not making any progress at all (red in the chart below).

Its housing component, the CPI for “services related to housing” decelerated a tad to +3.3%. It’s other services that consumers pay that are not related to housing that keep the services CPI nailed to 4.0%. The shaded area indicates the pre-pandemic range.

Housing-related services include actual rents paid by tenants; services for the maintenance and repair of dwellings; refuse and sewage costs; repair costs for furniture, furnishings, floor coverings, and appliances; domestic and household services; and insurance connected with the dwelling.

Worries about services inflation have for months cropped up the ECB’s announcement about its policy rates, which it has cut four times so far. This stubbornly high services inflation “reflects strong wage pressures and the fact that some services prices are still adjusting with a delay to the past inflation surge,” it said at its December 12 policy statement, when it nevertheless cut its deposit rate by another 25 basis points to 3.0%.

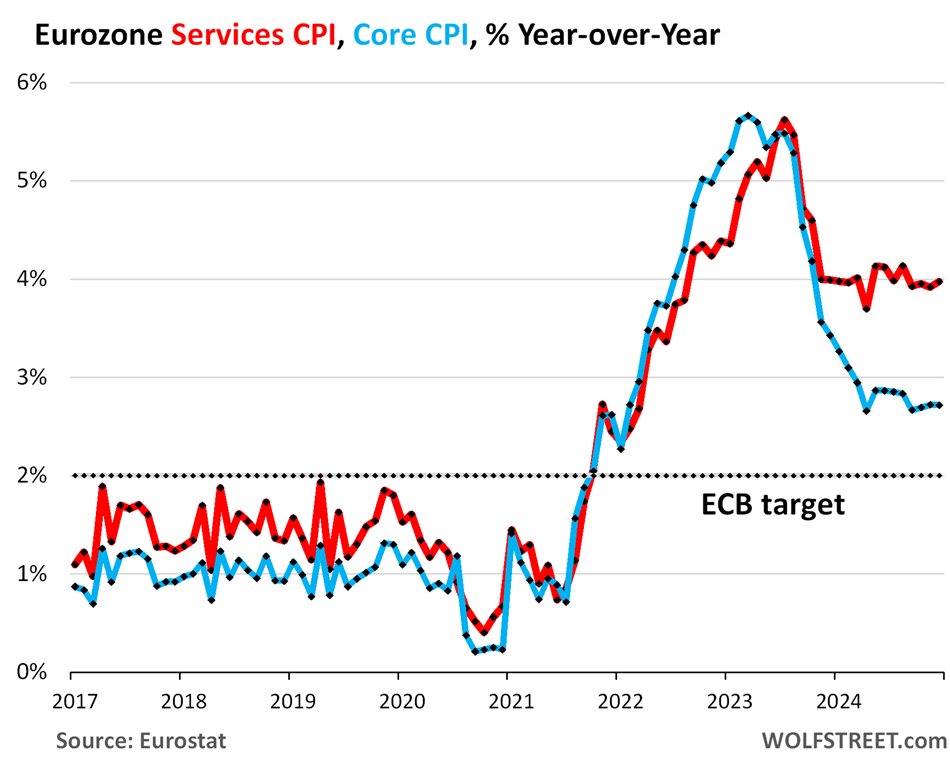

Core CPI – which excludes food, energy, tobacco, and alcohol products – rose by 2.7% in December and has been roughly in the same range for nine months and up a hair from April 2024.

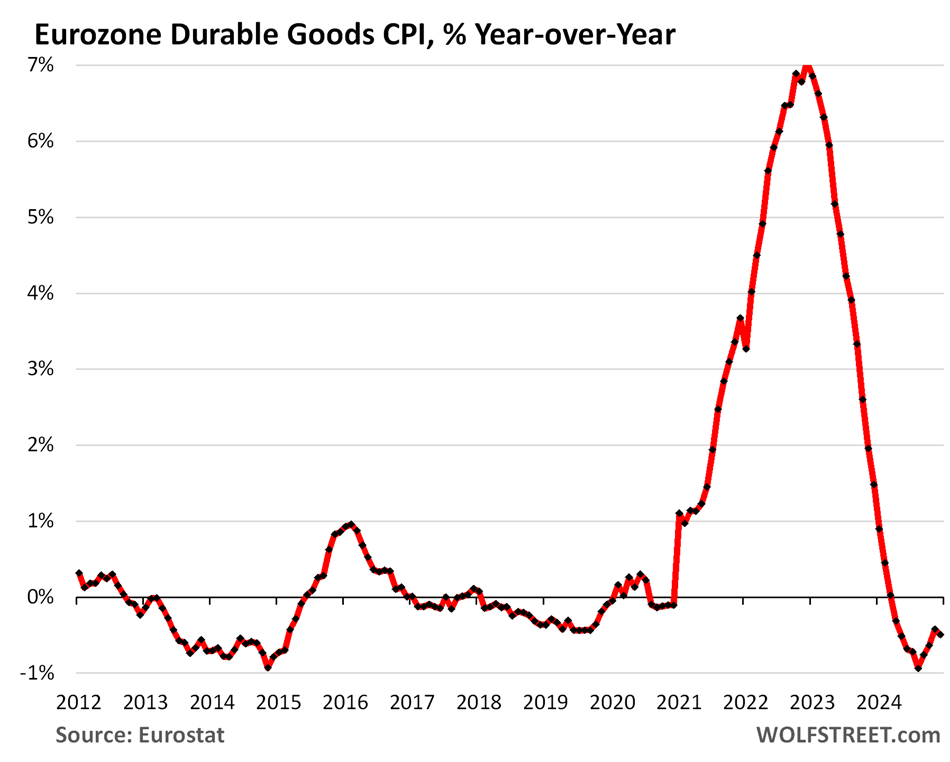

Core CPI is dominated by services, but also includes goods other than food, energy products, tobacco and alcohol. Prices of durable goods plunged off the pandemic spike and by early 2024 turned the year-over-year CPI of durable goods negative, this plunge in durable goods prices pulled down the core CPI.

But durable goods prices stopped plunging and over the past five months have ticked up again, which has been whittling down the year-over-year declines. If this trend continues and moves the year-over-year durable goods CPI into the positive, while services are stuck at 4%, then core CPI will accelerate away from the ECB’s target, rather than cool toward it.

Core CPI (blue), which has been running roughly in parallel with the services CPI (red) since April and not cooling any further, remains well above the ECB’s 2% inflation target for core and overall CPI (black dotted line). The ECB has been preaching for many months that core CPI would go back to 2%, while core CPI has refused to do so.

What had caused overall CPI for the Eurozone to cool substantially between mid-2022 and October 2024, were the plunge in energy prices off the huge spike, the drop in durable goods prices that had surged during the pandemic, and relative stability in food prices at very high levels. But now that honeymoon of cooling overall inflation is over.

Durables goods CPI rose over the past five months on a month-to-month basis, by 0.5% combined, which whittled down the year-over-year declines from earlier in 2024 to 0.5%. The spike in durable goods prices during the pandemic was caused by shortages and the accompanying price gouging, particularly with new and used vehicles, same as in the US:

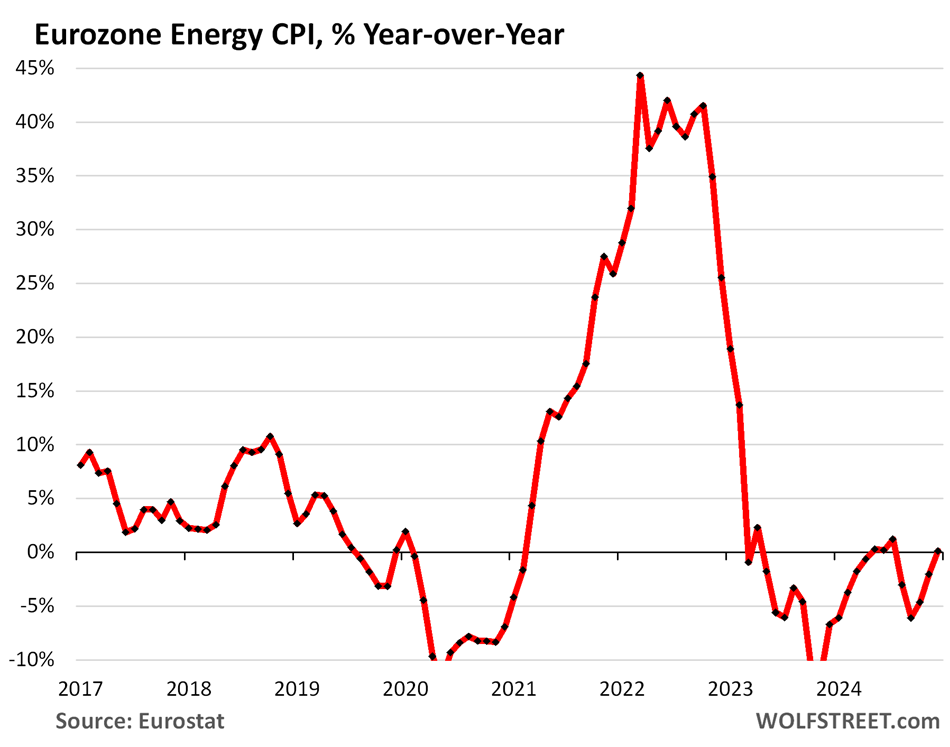

Energy CPI, which tracks prices for gasoline, diesel, natural gas, electricity, heating oil, etc., rose for the past three months, on a month-to-month basis, by a combined 1.5%, after sharp declines in the prior months. On a year-over-year basis, it is now unchanged.

Note the 45% year-over-year spike in mid-2022. This caused overall CPI to spike as well. Then came the plunge. In late 2023, the energy CPI was -11% year-over-year, and the negative readings mostly continue through November, but getting smaller.

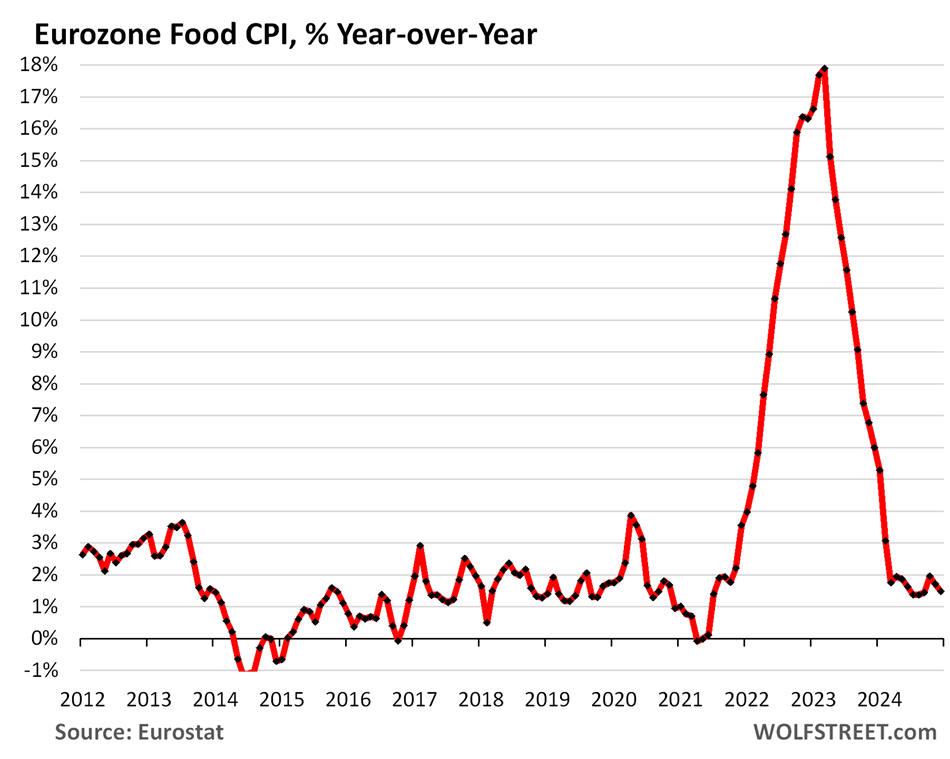

Food CPI, after a, 18% year-over-year spike into early 2023, has cooled substantially, rising by 1.5% year-over-year in December. This cooling of food inflation (the year-over-year rate of increases slowed form +18% to +1.5%, with prices at very high levels) has contributed to the cooling of overall CPI. But that’s now over too.

Overall CPI rose by 2.4%, the second acceleration in a row and is now roughly back where it had been 13 months earlier, in November 2023.

It had been pushed down by the plunge in energy prices (deeply negative year-over-year readings), the drop in durable goods prices (negative year-over-year readings), and the stabilizing food prices after the spike. On a year-over-year basis, all these three elements are in the process of ending or have already ended, which is why overall CPI has accelerated.

The chart below shows overall CPI (blue), core CPI (gold), and services CPI (red), along with the ECB’s target (black dotted line). Everything is above target, and not making any further progress, on the contrary.

The problem the ECB will run into is that further rate cuts will push the policy rates below the core CPI and overall CPI inflation rates, which is like throwing gasoline on a fire.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post ECB Faces a Problem: Euro Area Services Inflation Stuck at 4.0% for 13th Month. CPI Accelerates Further, as Energy & Durable Goods Stopped Plunging appeared first on Energy News Beat.

“}]]

Energy News Beat