[[{“value”:”

Quantitative Tightening has shed 25% of total assets from peak and 46% of pandemic QE.

By Wolf Richter for WOLF STREET.

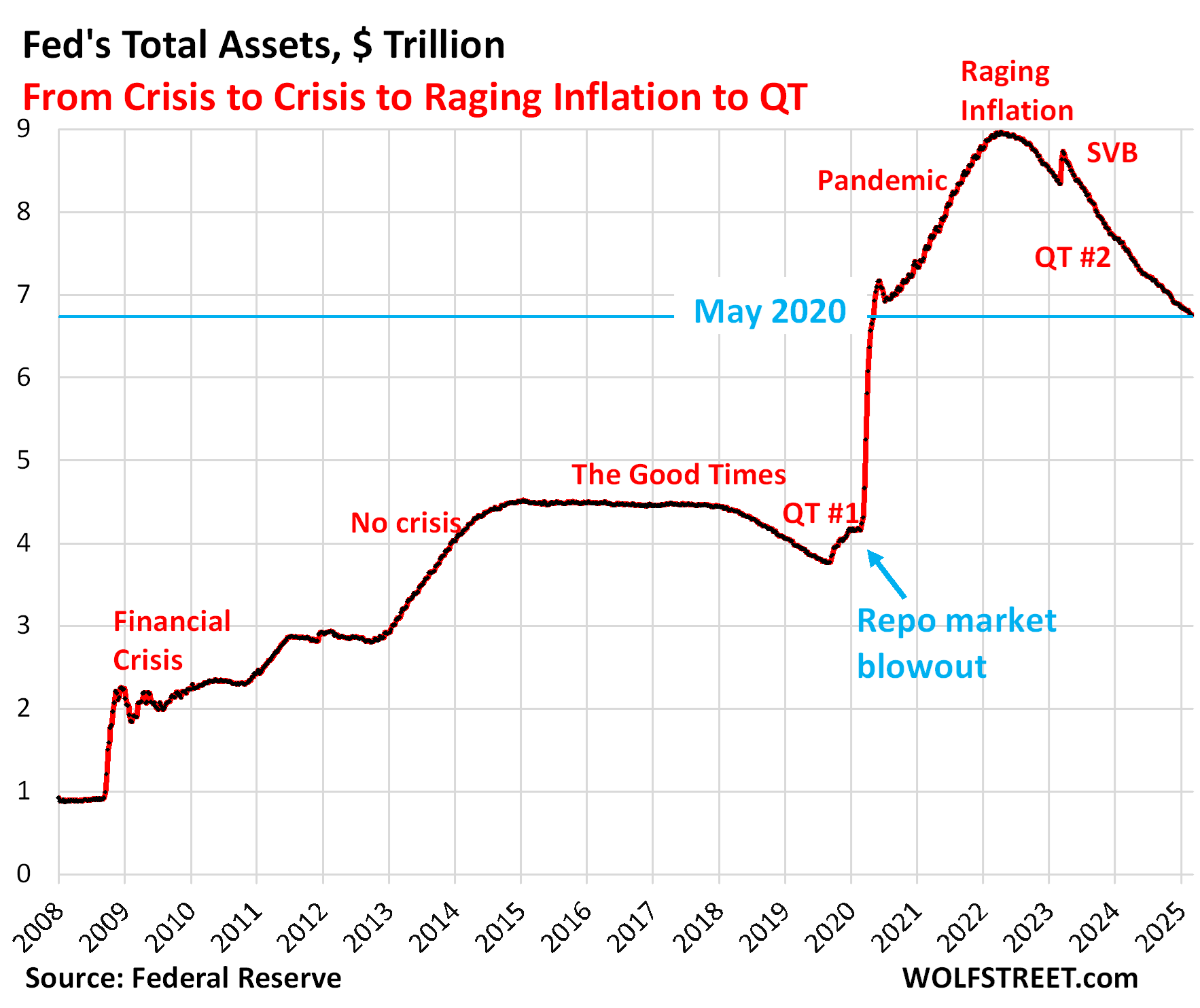

Total assets on the Fed’s balance sheet declined by $54 billion in February, to $6.76 trillion, the lowest since May 2020, according to the Fed’s weekly balance sheet today.

Since the end of QE in April 2022, the Fed has shed $2.21 trillion, or 25% of its assets. And it has shed 46% of the $4.81 trillion it piled on the balance sheet during pandemic QE from March 2020 through April 2022.

QT assets.

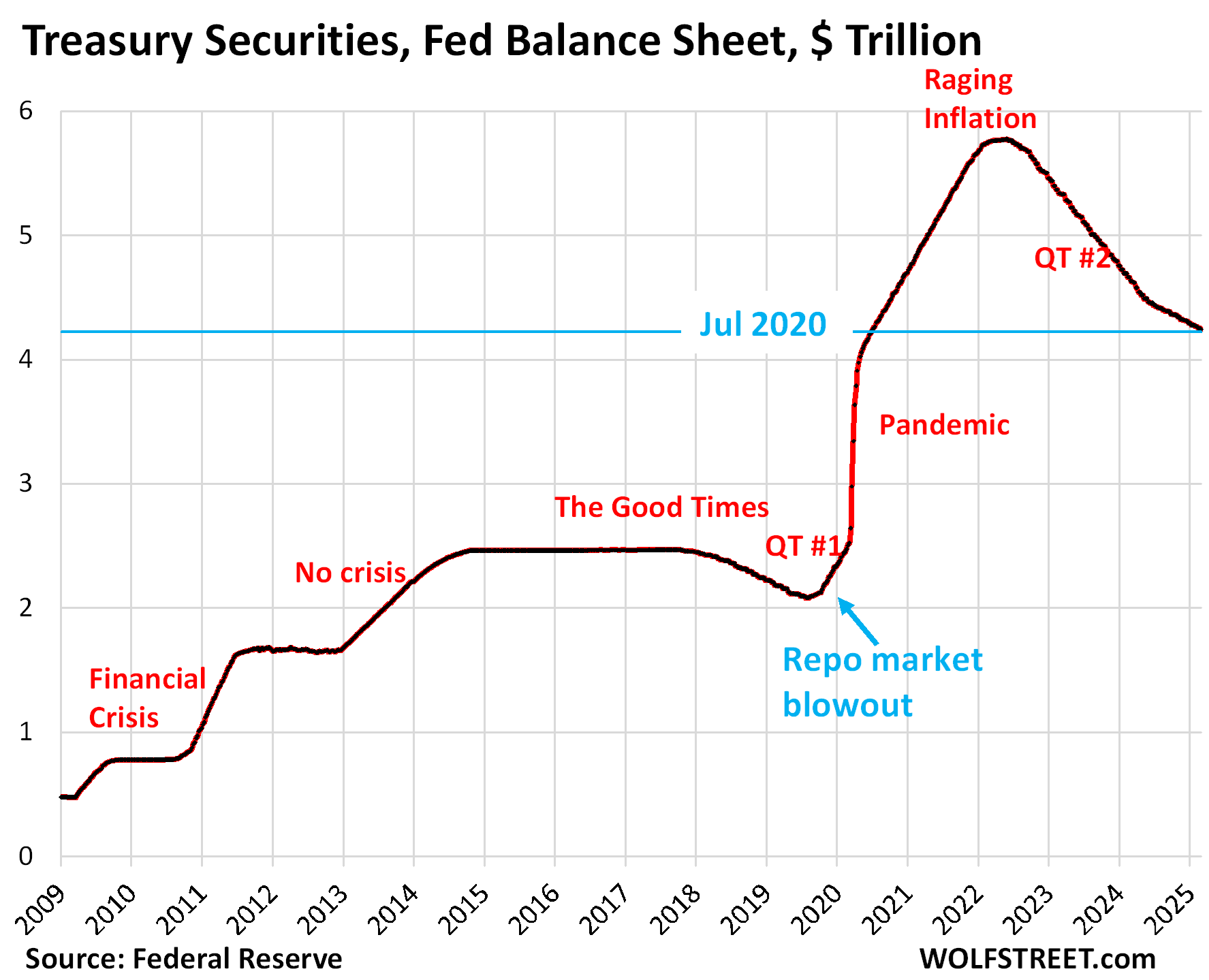

Treasury securities: -$24.3 billion in February, -$1.53 trillion from peak in June 2022, or -27% since the peak, to $4.24 trillion, the lowest since July 2020.

The Fed has shed 47% of the $3.27 trillion in Treasuries it piled on the balance sheet during pandemic QE.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. Since June 2024, the roll-off has been capped at $25 billion per month. About that much has been rolling off, minus the amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that is added to the principal of the TIPS.

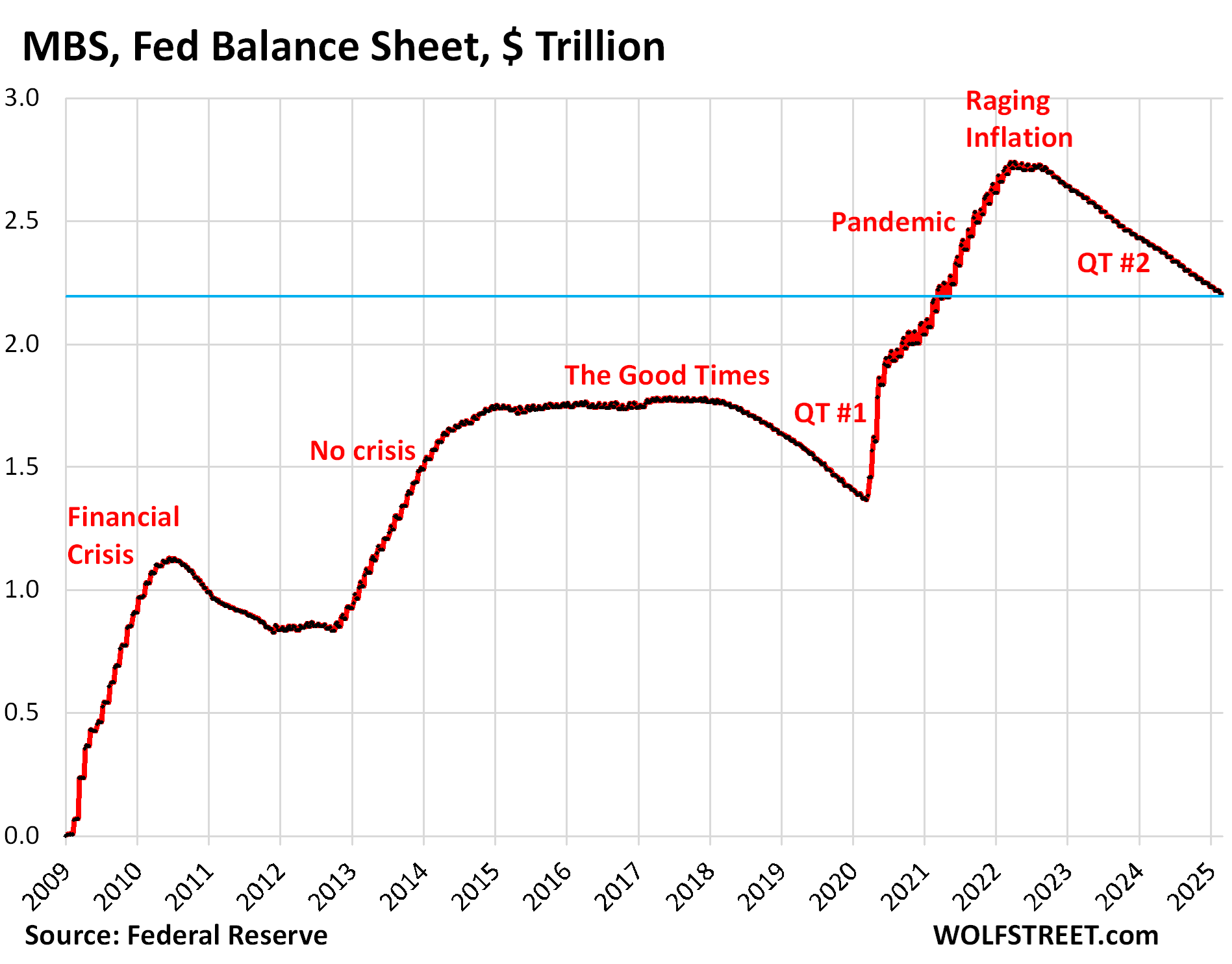

Mortgage-Backed Securities (MBS): -$14.2 billion in February, -$537 billion from the peak, to $2.20 trillion, first seen in March 2021.

The Fed has shed 19.6% of its MBS since the peak in April 2022, and 38% of the MBS it had piled on the balance sheet during Pandemic-QE.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But as sales of existing homes have plunged and mortgage refinancing has collapsed, far fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have become a trickle. As a result, MBS have come off the Fed’s balance sheet at a pace that has been mostly in the range of $14-17 billion a month.

The Fed is not exposed to credit losses if borrowers default on mortgages because it holds only “agency” MBS that are guaranteed by the government, where the taxpayer would eat those losses, not the Fed.

Bank liquidity facilities: inactive.

The Fed has five bank liquidity facilities. Four of them have either no balance at all anymore or a balance that is so small by the Fed’s scale that’s essentially zero. All of them were heavily used after the SVB collapse, and two of them – the FDIC facility and the BTFP – were specifically set up to deal with the SVB fallout but are now shut down.

- Central Bank Liquidity Swaps ($133 million)

- Repos ($84 as of the close of the balance sheet on Wednesday evening, today at $0)

- Loans to the FDIC ($0).

- Bank Term Funding Program BTFP ($79 million in remaining loans to be repaid by March 11).

- Discount Window: unchanged in February at $3.1 billion. Qualifies as “near zero” as during the SVB panic, it had spiked to $153 billion.

What else caused total assets on the balance sheet to drop?

The balance sheet declined in total by $54 billion in February. Above, we accounted for $38.7 billion:

- Treasury securities: -$24.4 billion

- MBS: -$14.3 billion

And another $16 billion came off the balance sheet in February largely in these two accounts:

“Other assets” fell by $14 billion. This consisted mostly of accrued interest on its bond holdings that the Fed had set up as a receivable (an asset), and that it got paid in February, which reduced the receivable. When it gets paid interest, the Fed destroys that money (the Fed doesn’t have a “cash” account, like companies do; it creates money when it pays for something and destroys money when it gets paid). By destroying the cash, the Fed reduces its assets.

Conversely, when it accrues the interest it earned before it receives it, it increases its assets. So the balance moves up and down on a weekly basis in a range currently between $28 billion and $47 billion.

Since this account also includes “bank premises” and other accounts receivables, it will always have a balance.

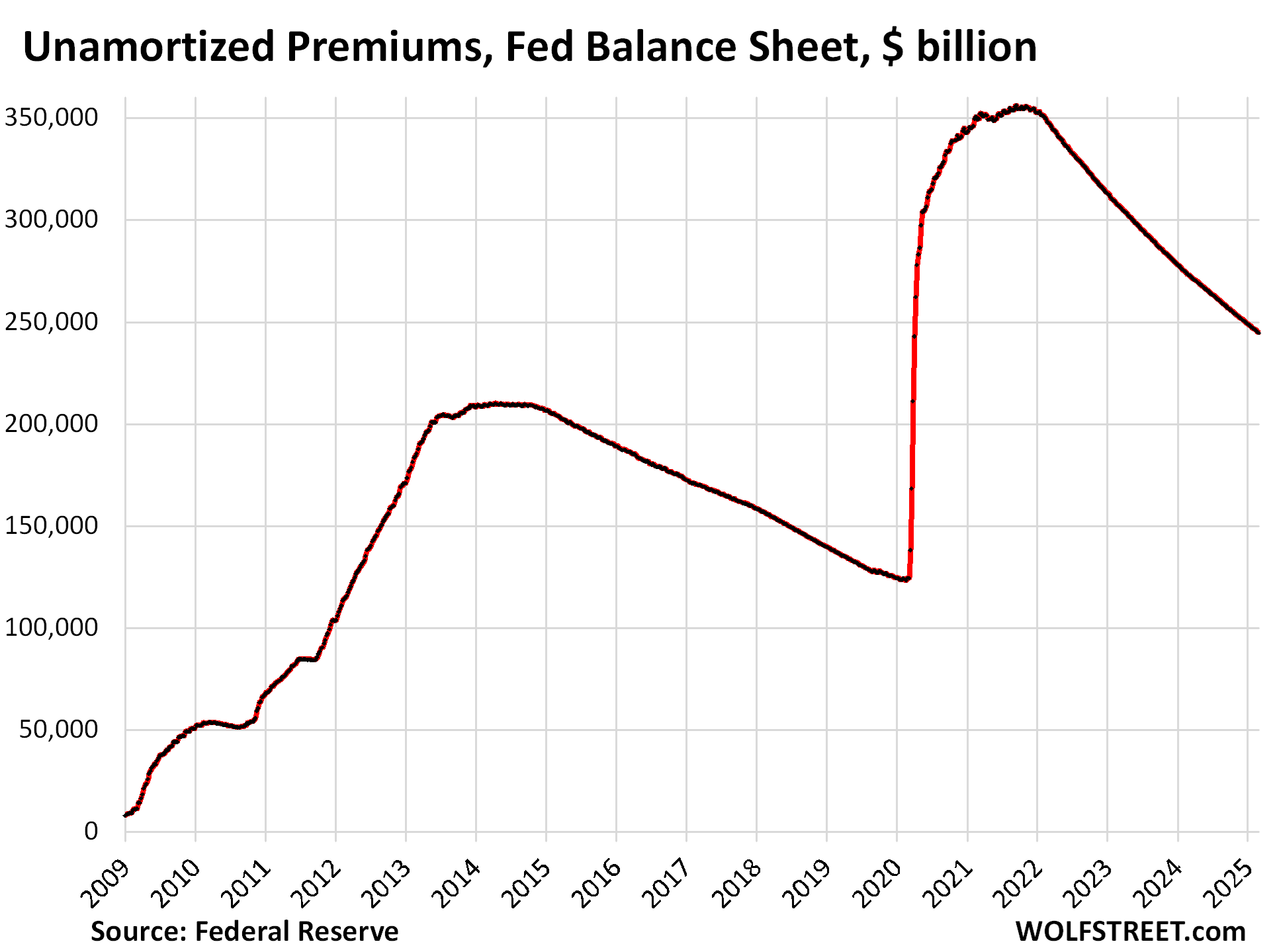

“Unamortized premiums”: $2.1 billion. This is the regular amount the Fed writes off every month to account for the premium over face value it had to pay for bonds during QE that had been issued with higher coupon interest rates earlier and that had gained value as yields dropped before the Fed bought them. Like all institutional bondholders, the Fed amortizes that premium over the life of the bond. The remaining balance of unamortized premiums is now down to $245 billion, from $356 billion at the peak in November 2021:

And it case you missed it: The Future of the Fed’s Balance Sheet: Fed’s Logan on How Assets Might Shift from Longer-Term Securities to Short-Term T-Bills, Repos, and Loans after QT Ends. MBS Entirely Off the List

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Fed Balance Sheet QT: -$54 Billion in February, -$2.21 Trillion from Peak, to $6.76 Trillion, Lowest since May 2020 appeared first on Energy News Beat.

“}]]

Energy News Beat