[[{“value”:”

Since September, the Fed cut by 100 basis points while the 10-year Treasury yield rose by 87 basis points! There are now doubts about further cuts.

By Wolf Richter for WOLF STREET.

When the Fed cut its policy rates on Wednesday by 25 basis points, it laid out a scenario of higher inflation and higher “longer-run” policy rates, and projected only two rate cuts in 2025, half the rate cuts it projected three months ago.

Then, to top it off, people who listened to Powell at the press conference walked away thinking that there might not be any rate cuts next year, that the “recalibration” phase of the Fed’s monetary policy was already finished after only 100 basis points in cuts, and that we may be on the cusp of a new phase.

As this emerged on Wednesday, the S&P 500 index tanked 3%. And the Treasury market is showing this thinking.

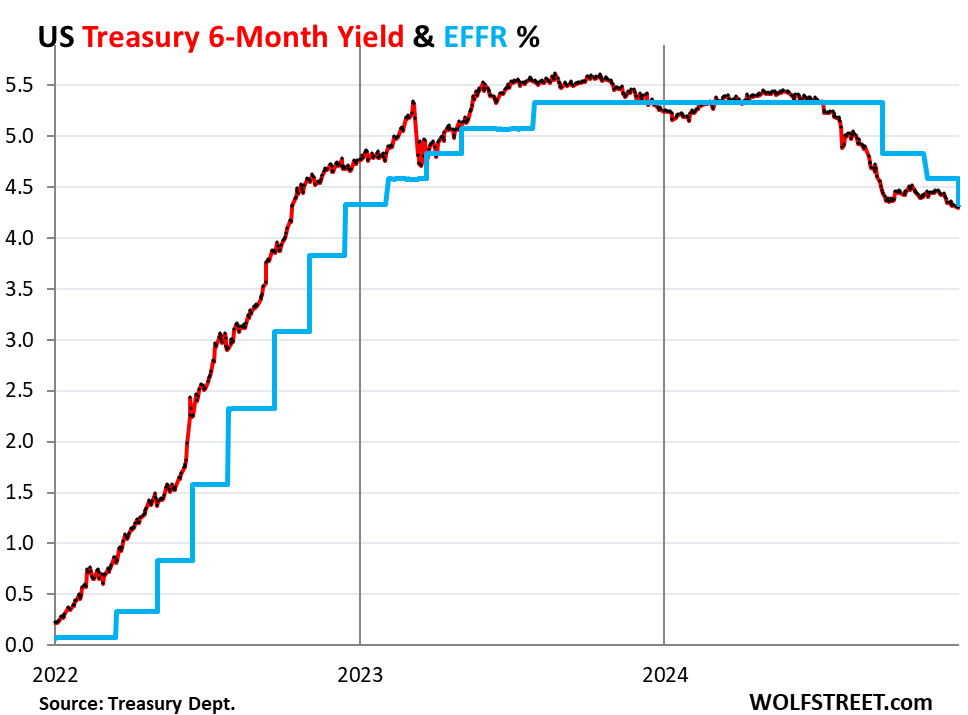

Short-term yields didn’t fall at all this week. The rate cut was already 100% priced in, and now there is no more rate cut priced in within the short-term window of those securities. On Friday December 13, the yields of 1 to 6 months were all at 4.30% to 4.33%. And that’s where they also ended up on Friday December 20.

And they’re now right at the Effective Federal Funds Rate (4.33% after the rate cut), which the Fed targets with its policy rates.

The 6-month Treasury yield sees no rate cut within its window. It had priced in each of the three rate cuts about two months in advance. It also priced in the rate hikes in 2022 and 2023 with a similar advance. During the March 2023 banking crisis, it briefly saw a pause that didn’t come. And in January 2024, it started pricing in a rate cut but then gave up on it. Now it has settled into a no-rate cut scenario within its window over the next few months:

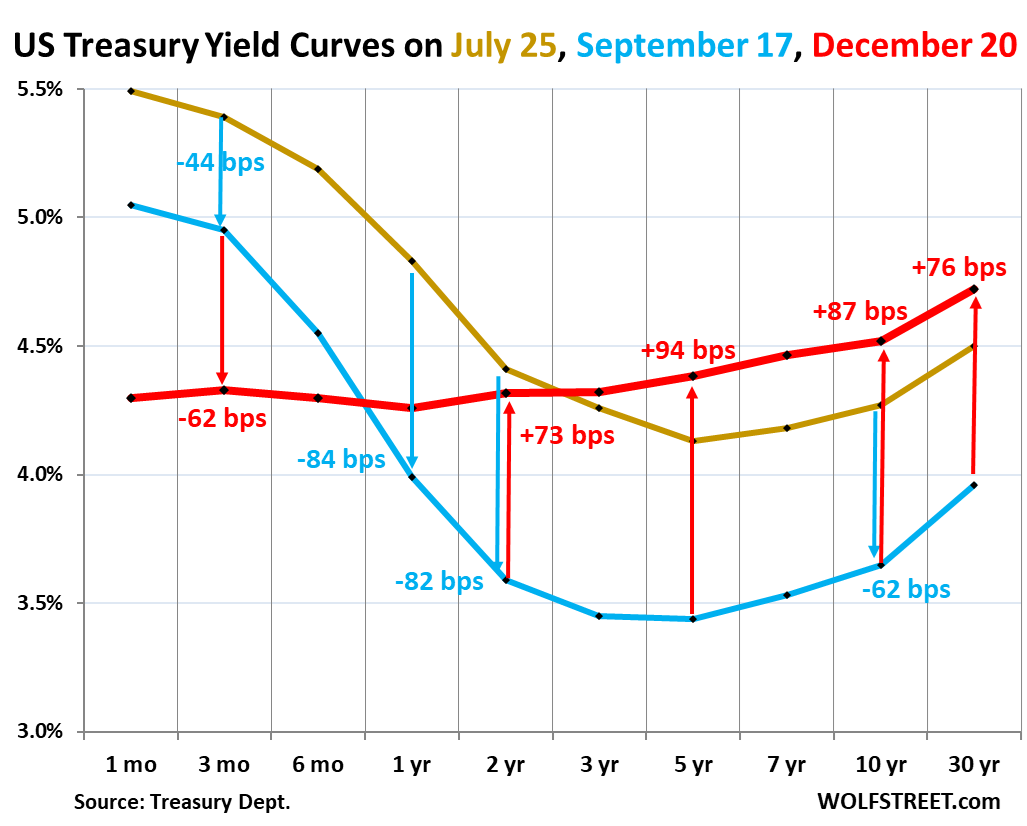

The yield curve un-inverted entirely.

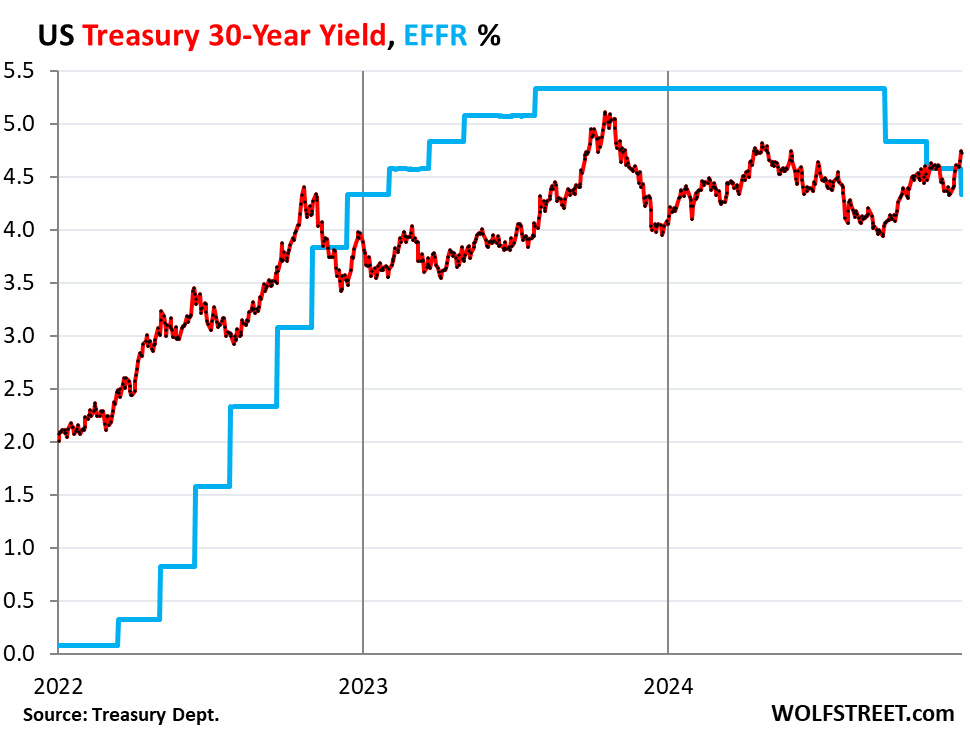

While short-term yields stayed roughly put during the week, everything from the 1-year yield and longer rose. At the long end, the 10-year yield rose by 12 basis points to 4.52% and the 30-year yield rose by 11 basis points to 4.72%.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data spiraled down (which was a false alarm).

- Blue: September 17, 2024, the day before the Fed’s rate cuts started.

- Red: Friday, December 20, 2024.

The yield curve had inverted in July 2022, when the Fed’s big rate hikes pushed up short-term Treasury yields very fast, but longer-term yields rose more slowly, and so the short-term yields blew past them.

But the yield curve is still fairly flat, with only a 22-basis point spread between the 2-year yield and the 10-year yield. Over time, as the yield curve normalizes, it will steepen, and the 2-to-10-year spread will widen. This could happen in two ways: With shorter-term yields falling or with long-term yields rising, or both.

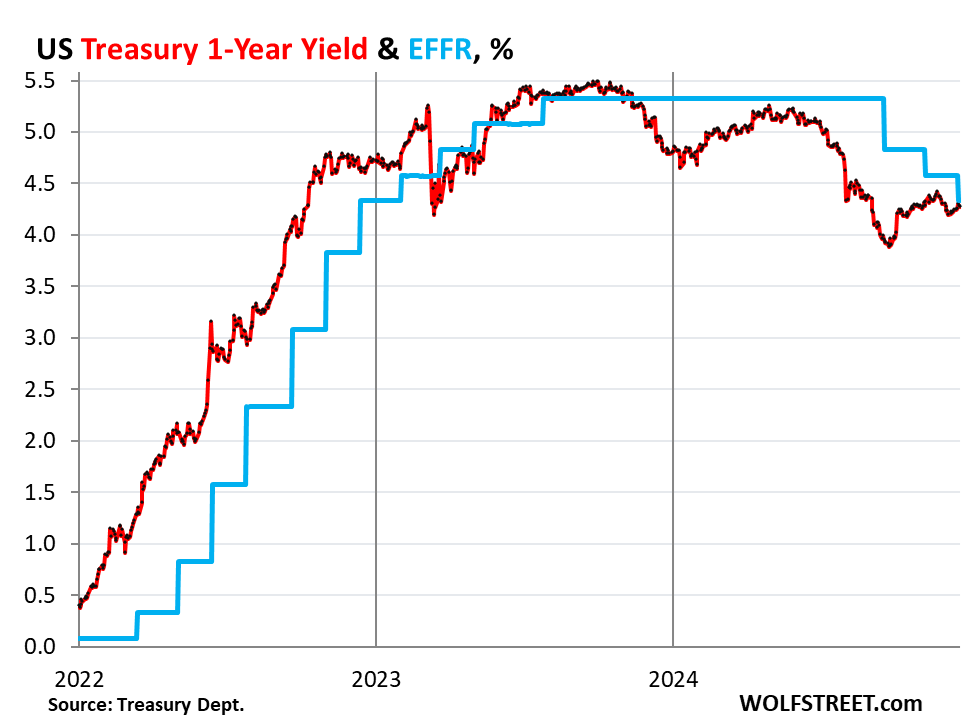

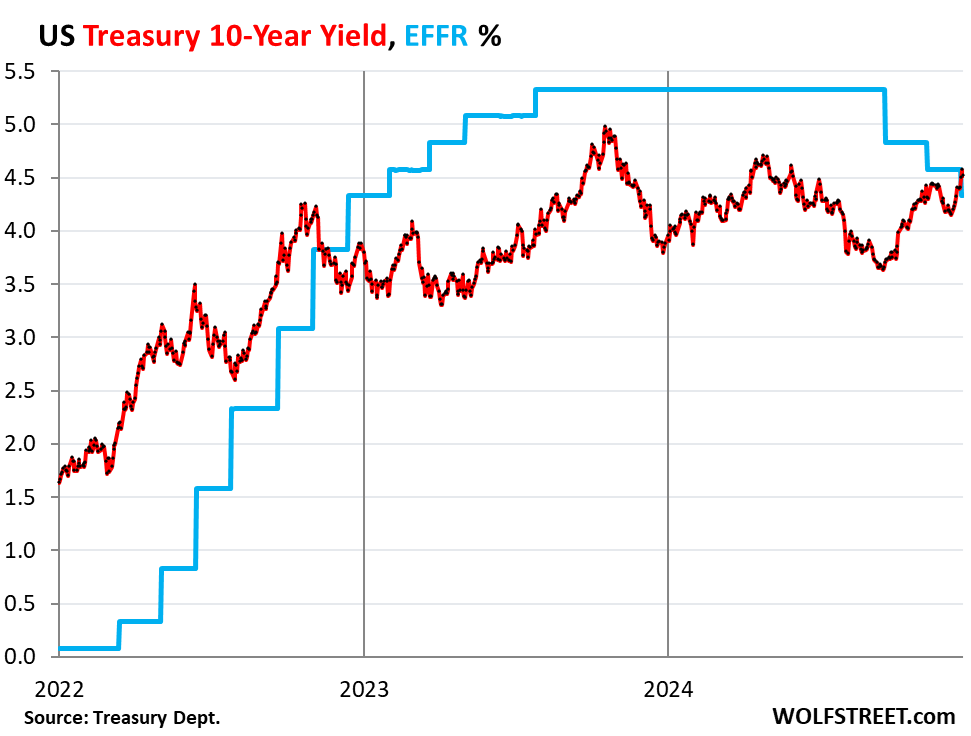

Yields v. the Effective Federal Funds Rate.

On Wednesday, the Fed cut its target range for the EFFR to 4.25% to 4.50%. The EFFR then dropped from 4.58% to 4.33% (blue in the charts below). And here is how Treasury yields of 1-year and longer reacted.

The 1-year Treasury yield, 4.26%, 7 basis points below EFFR:

The 2-year Treasury yield, 4.32%, at about the EFFR:

The 10-year Treasury yield, 4.52%, 19 basis points above EFFR:

The 30-year Treasury yield, 4.72%, 39 basis points above the EFFR:

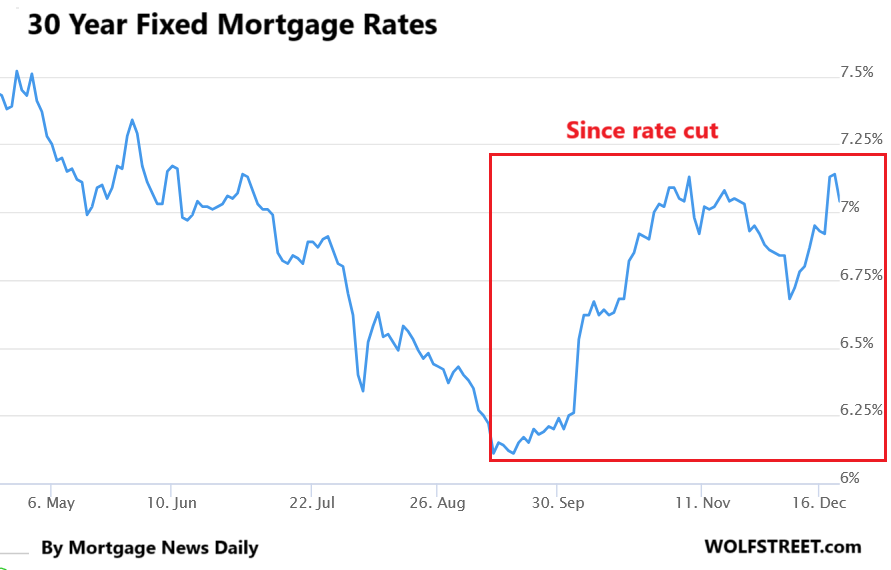

Mortgage rates back above 7%.

Since the initial rate cut in September, the average 30-year fixed mortgage rate has risen by nearly 1 percentage point, from 6.11% to 7.04%, according to the daily measure from Mortgage News Daily.

It roughly parallels the 10-year yield, but is higher, and that spread between them varies but is fairly wide currently due to some factors that we analyzed here. A wider spread and a higher 10-year Treasury yield means higher mortgage rates. So maybe it’s time to get re-used to these kinds of mortgage rates that were normal before 2008.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Treasury Yield Curve Un-Inverts Entirely, as Long-Term Yields Rise while Short-Term Yields Stay Put, No Longer Pricing in Rate Cuts. Mortgage Rates back Above 7% appeared first on Energy News Beat.

“}]]

Energy News Beat