While China keeps regurgitating the same tired and trite line about an “imminent” fiscal and housing stimulus, which reportedly is in the “trillions” of yuan, yet which to date is entirely imaginary and never actually materalizes, its housing market continues to crater and will soon reach a point where a depression is unavoidable… at which point the all too real stimulus to reboot the economy will be in the tens of trillions.

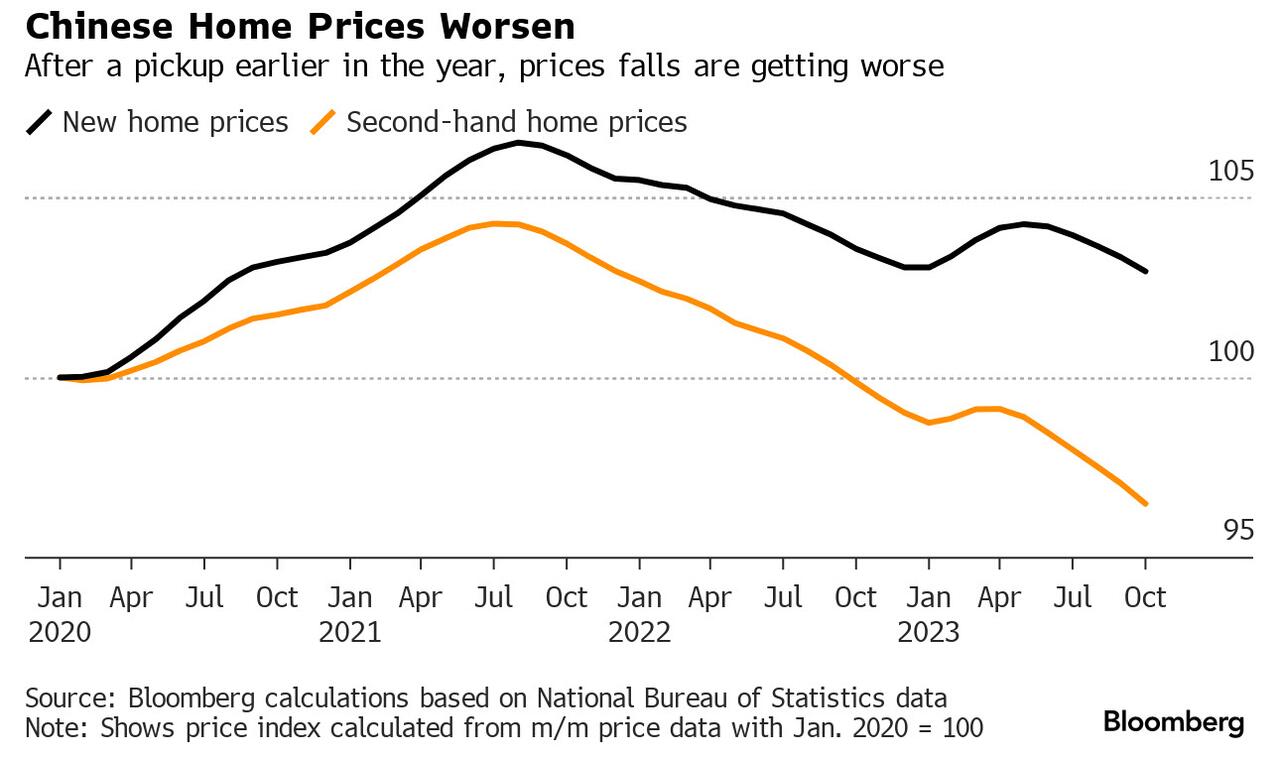

Overnight, China’s National Bureau of Statistics reported that last month, China’s home prices fell the most in eight years signaling the property slump is worsening even after the government ramped up efforts to revive demand. In fact, one can argue that central planning is merely doing what it always does: makes the situation even worse.

New-home prices in 70 cities, excluding state-subsidized housing, declined 0.38% last month from September, when they dropped 0.3%, official figures showed Thursday. The decrease was the steepest since February 2015.

{kind=link}

The drop adds to further evidence of a relentless and persistent housing downturn after official figures this week showed a contraction in sales and property investment deepened. Fresh stimulus measures rolled out at major cities since August, and which have been derided as much too small to make an impact, have done little to turn around the sector, which is dragging on China’s economic recovery and which has traditionally served as the primary source of wealth for China’s middle class.

While prices in the largest, tier-1 cities, slid 0.35%, sharply deteriorating from a 0.05% decrease a month earlier, tier-2 cities, mostly provincial capitals, fared better with a narrower price decline amid an easing in homebuying restrictions.

The second-hand market didn’t fare any better, with prices tumbling 0.58%, the most since October 2014. A Bloomberg Intelligence gauge of Chinese property developers fell as much as 1.4% on Thursday morning, extending this year’s decline to 43%.

Here are some more details:

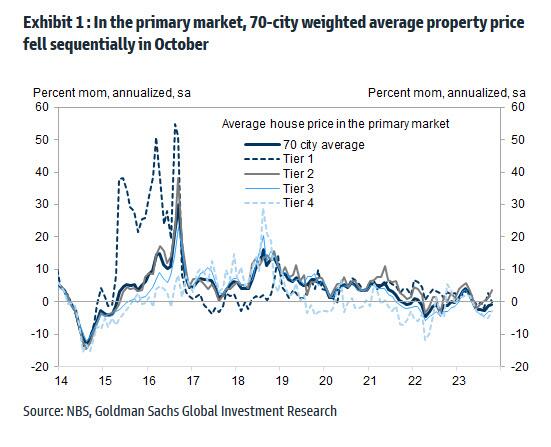

After seasonal adjustments, weighted average house prices in the primary market declined by 0.9% mom annualized in October, despite ongoing easing policies.

{kind=link}

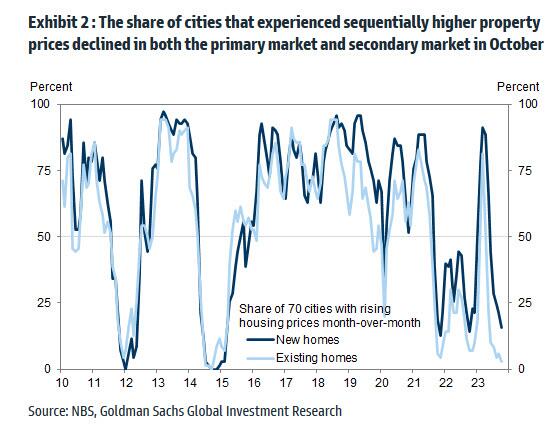

The proportion of cities that experienced sequential house price gains declined in both the primary market and secondary market in October from September. New home prices dropped in 56 of 70 cities in October. Second-hand home prices fell in 67 cities, with just Xi’an in Shaanxi province and Hangzhou in Zhejiang showing growth.

{kind=link}

Most property-related activity remained sluggish in year-on-year terms in October. 30-city new home transaction volume declined by 27.1% yoy month-to-date in November. Major cities’ inventory months (sellable gross floor area divided by 12-month rolling gross floor area sold) rose to 23.8 in October from 22.7 in September, with the increase mostly led by Tier-3 cities.

A brief housing market rebound earlier this year after China’s post-Covid reopening “turned out to be short-lived,” said Chen Wenjing, associate research director at China Index Holdings. “Homebuyers are deterred by squeezed incomes and the uncertain property market outlook.” The record high youth unemployment, which forced Beijing to suspend the data series once it crossed above 21%, is not helping.

Meanwhile, the latest October money and credit data suggested growth of household medium-to-long term loans, which are mostly mortgages, decelerated in sequential terms in October from September.

In the latest (insufficient) move to prop up the real estate sector, Bloomberg reported that Beijing is planning to provide at least 1 trillion yuan ($138 billion) of low-cost financing to urban village renovation and affordable housing programs. While details of the new plan remain unclear, some economists say it will be even less effective than earlier efforts. The new programs would mostly take place in some of the largest metropolitan areas, outside the low-tier cities where the slump is most severe.

Following the slew of easing announcements on property policy, Goldman economists expect more housing easing measures in coming months, including more relaxation of home purchase restrictions in large cities, among others. However, considering persistent property weakness related to lower-tier cities and private developers, such easing measures may only lead to an “L-shaped” recovery in the sector in coming years. In other words, no recovery.

As is widely known by now, China’s property crisis has engulfed almost all of the largest developers, which have been struggling to repay debts and complete projects since a credit crunch emerged three years ago. China Vanke, one of the country’s few remaining investment-grade builders, saw its dollar bonds plunge in recent weeks on the heels of industry giant Country Garden’s default. Vanke later received an unusually strong show of support from the local government.

“Property remains the biggest drag amid the rising credit risk among developers,” Larry Hu, head of China economics at Macquarie Group Ltd., wrote in a note this week.

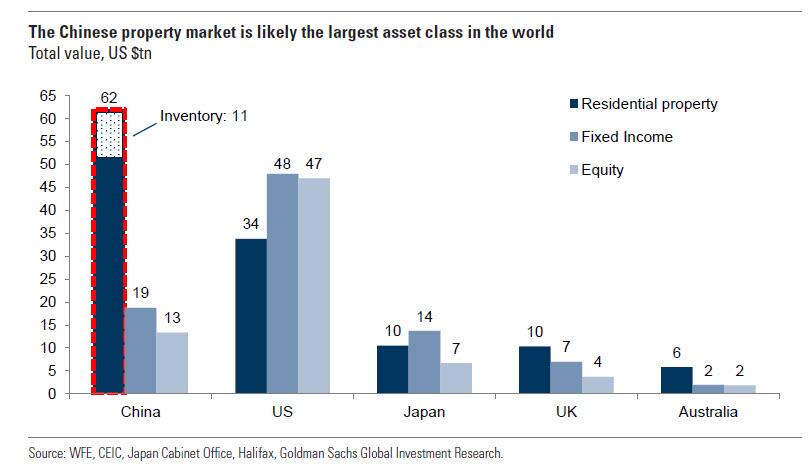

As a reminder, two years ago, Goldman calculated that China’s housing market is the world’s single biggest asset class…

{kind=link}

… however, after the spectacular implosion of the past two years, it is unclear where it ranks today.

Loading…

The post China Home Prices Plunge The Most In Eight Years appeared first on Energy News Beat.

Energy News Beat