[[{“value”:”

The aggressive Bash-Down by the White House of long-term Treasury yields and the dollar since January worked. Until it didn’t.

By Wolf Richter for WOLF STREET.

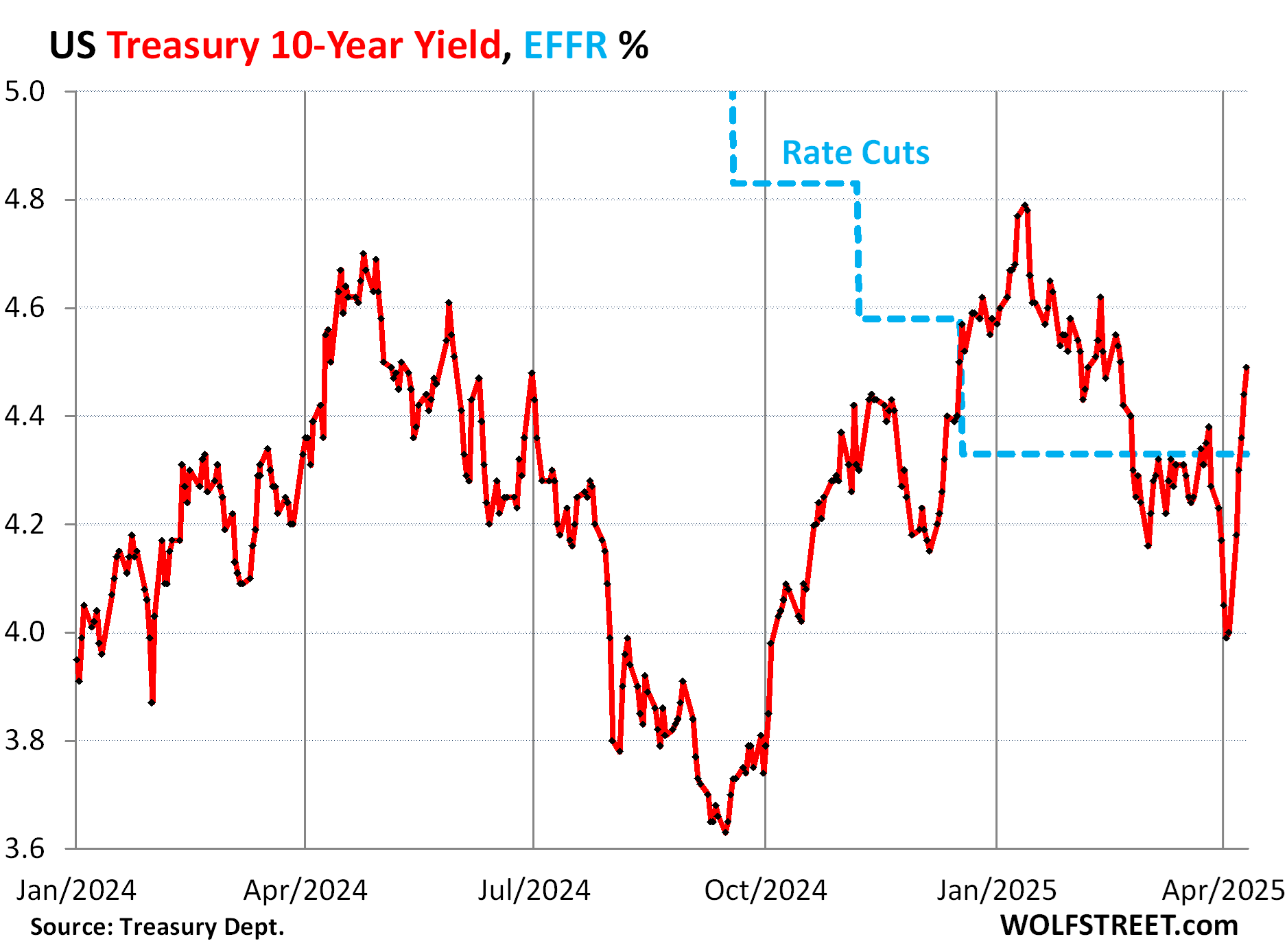

The 10-year Treasury yield rose to 4.49% on Friday, back where it had been on February 20. It has snapped back by 50 basis points from the recent low on April 3 of 3.99%, after a long hard plunge.

By comparison: Starting in mid-September, the 10-year Treasury yield surged by 116 basis points to 4.79% on January 10, 2025, and there was no talk of an impending catastrophe. But now that the 10-year yield has risen by only 50 basis points, to only 4.49%, and is once again barely above the effective federal funds rate (blue in the chart below), the media – pushed by the crybabies on Wall Street – is generating piles of scary headlines about an impending catastrophe?

Starting in January, Treasury Secretary Scott Bessent began actively bashing down long-term Treasury Yields and the dollar. Lower long-term yields would translate into lower funding costs for the US economy. And a weaker dollar would boost the economy by favoring exports (a positive in GDP) over imports (a negative in GDP). This was the explicit two-pronged effort by the White House to give the economy a boost. And the bash-down worked. Until it didn’t.

The bash-down caused the 10-year Treasury yield to careen down 80 basis points, from its recent high on January 10 of 4.79% to 3.99% on April 3. That was a lot very fast.

But there was an issue with this bash-down of the yield: Inflation is sticking around, and may be accelerating further, and the Fed is expecting higher inflation rates going forward based on the tariffs. Future inflation rates might be in the 3% range or higher. The long-term Treasury market fears out-of-whack inflation more than anything.

But amid the bash-down, the 10-year Treasury yield went from 4.79% in January – already somewhat unappetizing in this inflationary environment – to outright gross at 3.99% on April 3. And then investors lost interest at these low yields. Yields had to shoot up to where the buyers were, and so the 10-year yields snapped back after having been push down too far, and on Friday closed at 4.49%.

That higher yield brought out demand, including foreign demand.

At the 10-year Treasury auction on Wednesday, there was very strong demand from indirect bidders, which include foreign buyers, including foreign central banks. The auction was described as “stellar.” The $39 billion in notes were sold at a yield of 4.435%.

Then on Thursday, there was the “stellar” 30-year Treasury auction, where $22 billion in 30-year bonds were sold at a yield of 4.813%, amid very strong demand from indirect bidders which include foreign investors.

So the White-House bash-down of the 10-year Treasury yield worked until it didn’t, as the market ran out of investors that want to commit funds for 10-years at 4%. But at the current yields, investors scrambled to buy at the auctions.

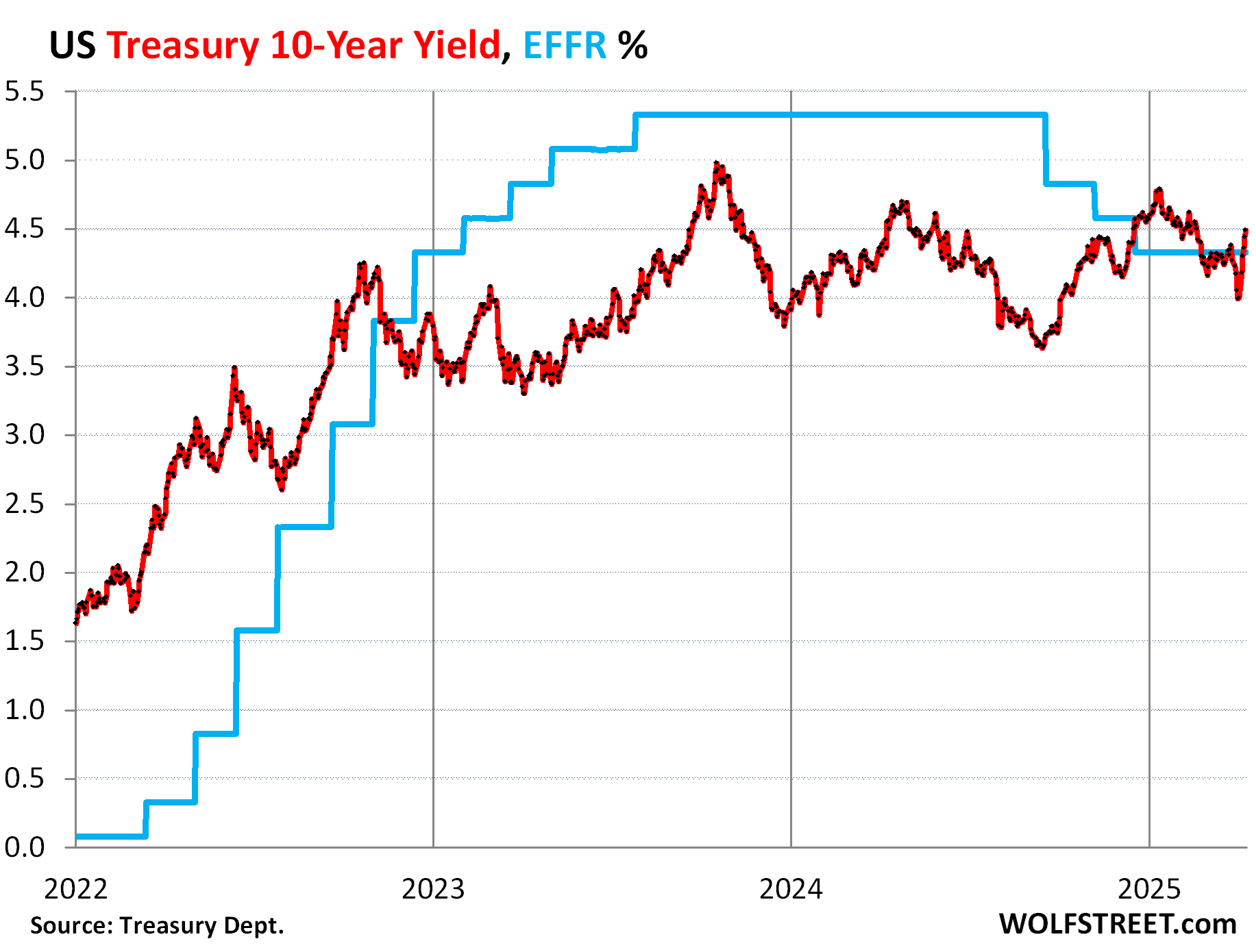

The longer view going back to 2022 shows just how funny the fretting in the media and by the Wall Street crybabies is. The recent snap-back of the 10-year Treasury yield put it back above the EFFR, where it should be in this inflationary environment. It should have never dropped to 3.99%:

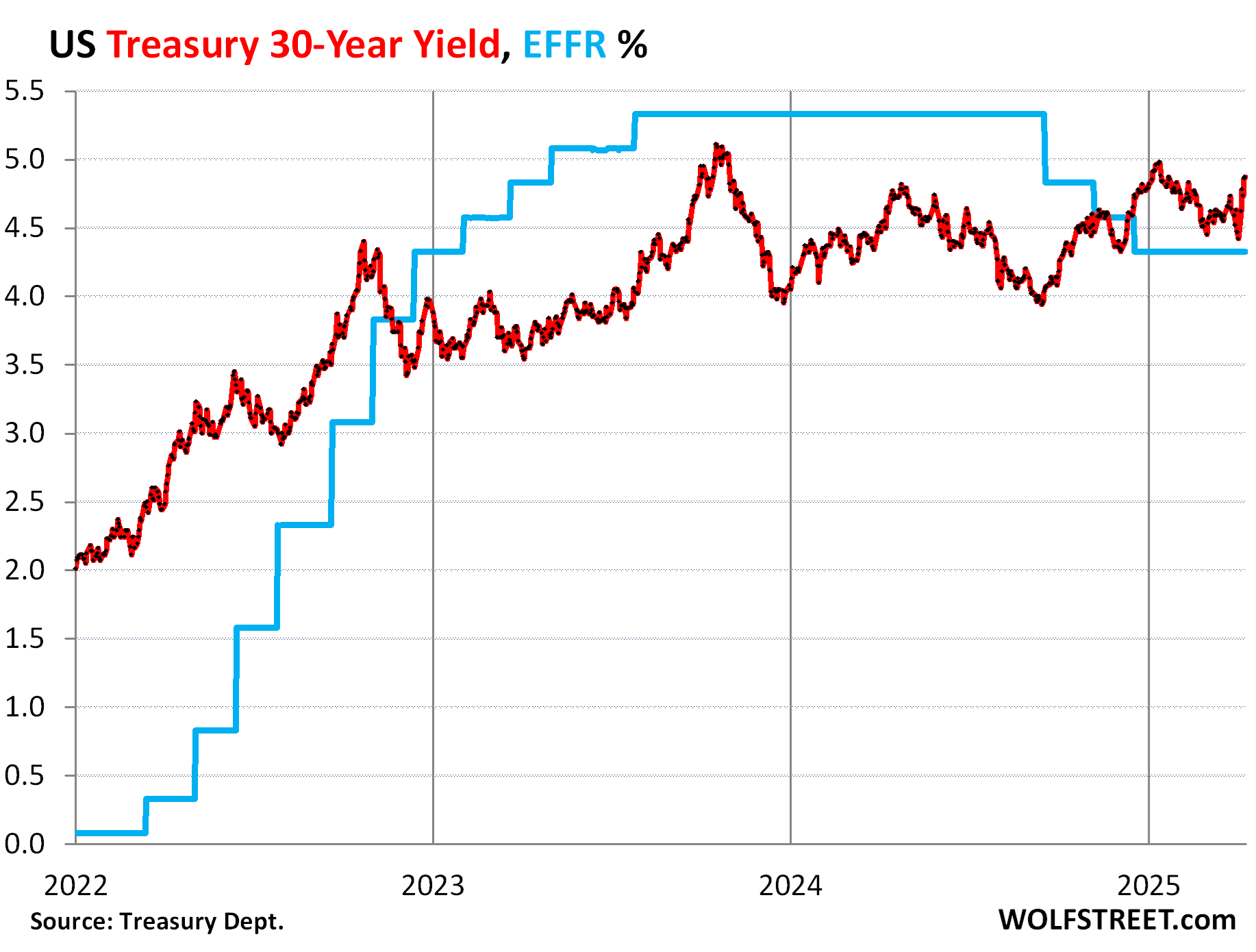

The 30-year Treasury yield closed at 4.87% on Friday, back where it had been on January 31, and below the near 5%-rate on January 10, and well below the 5%-plus range where it had been in October 2023.

It has traded in a fairly narrow range since mid-2023, and the recent snap-back from the drop, when seen over this time frame, wasn’t much to write home about.

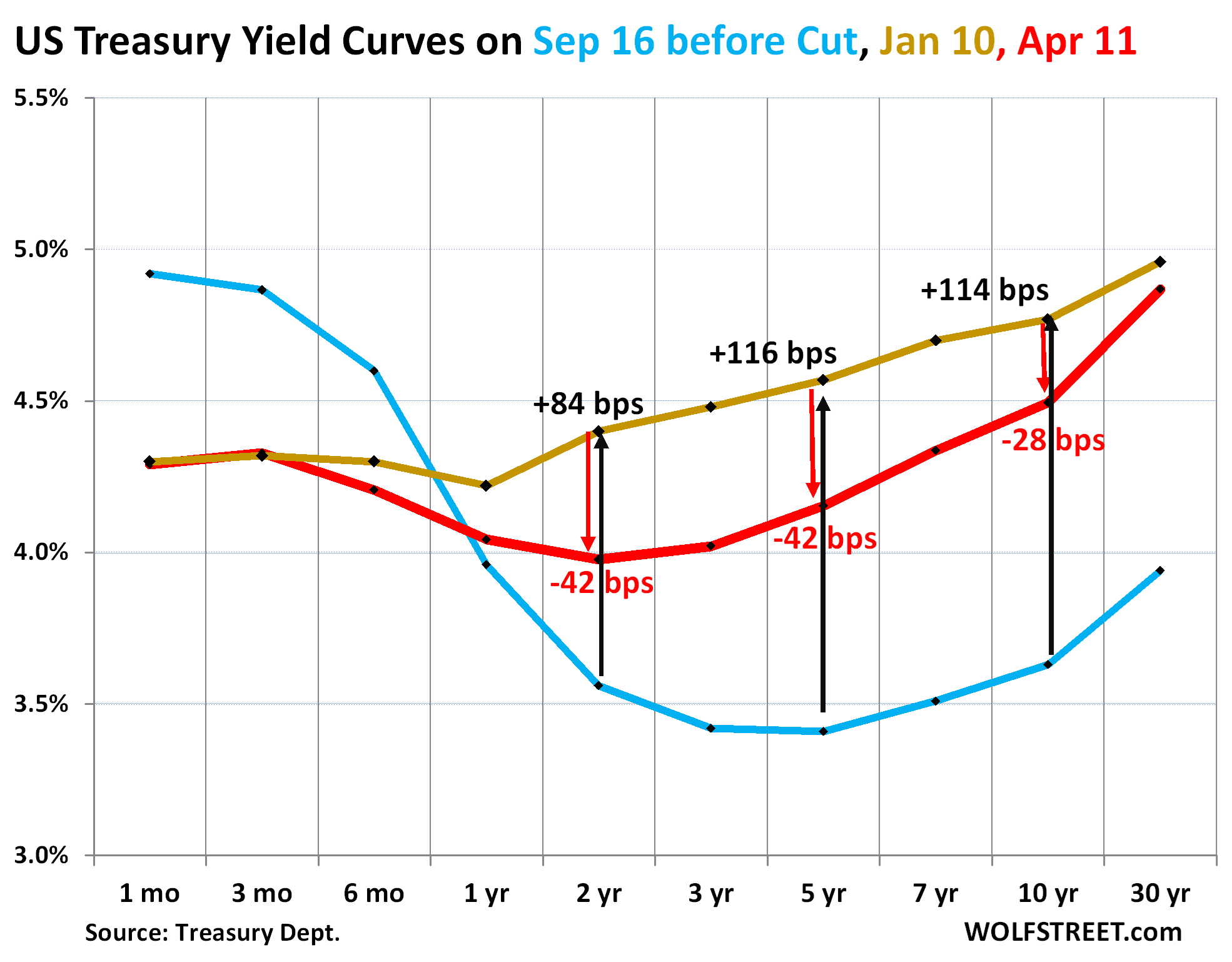

Yield curve re-un-inverted, still with a sag in the middle.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Red: April 11, 2025.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

Rate cuts are on ice, and so short-term yields haven’t moved much and remain glued to the EFFR.

Longer-term yields have snapped back from the recent lows, but are still lower than on January 10.

As a result, yields of 7 years and longer are now once again higher than short-term yields, and that part of the yield curve has re-un-inverted. But there is still this sag in the middle, though it is shallower than it was two weeks ago.

In a Treasury market that doesn’t get aggressively bashed down by the White House, longer-term yields in this inflationary environment should be higher than they’re now. A 10-year yield of about 5% and a 30-year yield north of that would look about right, in my view.

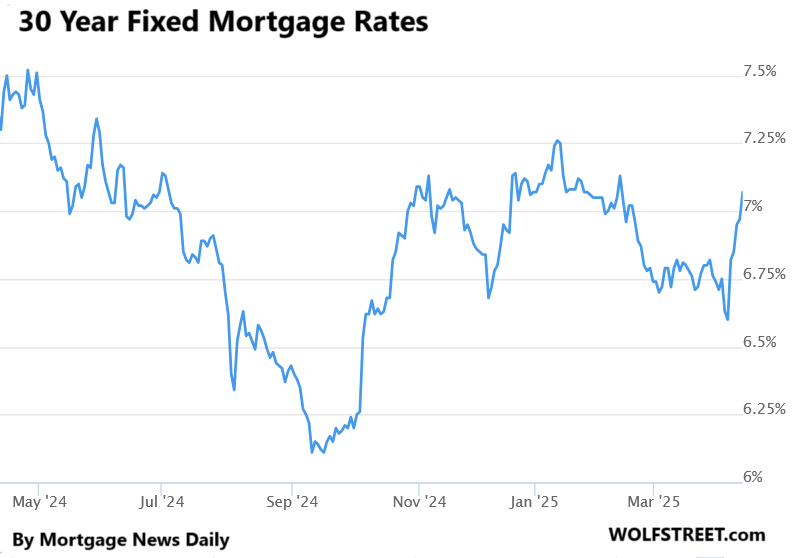

Mortgage rates are back over 7%.

The 30-year fixed mortgage rate roughly tracks the 10-year Treasury yield, but is higher, and that spread between the two varies.

Following the White-House interest-rate bash-down, mortgage rates fell with the 10-year yield, and now they too snapped back.

The average 30-year fixed mortgage rate on Friday rose to 7.07%, according to the daily measure by Mortgage News Daily. In the era before QE started, 7% mortgage rates were at the low end. In today’s inflationary environment, 7%-plus mortgage rates are somewhere close to reasonable.

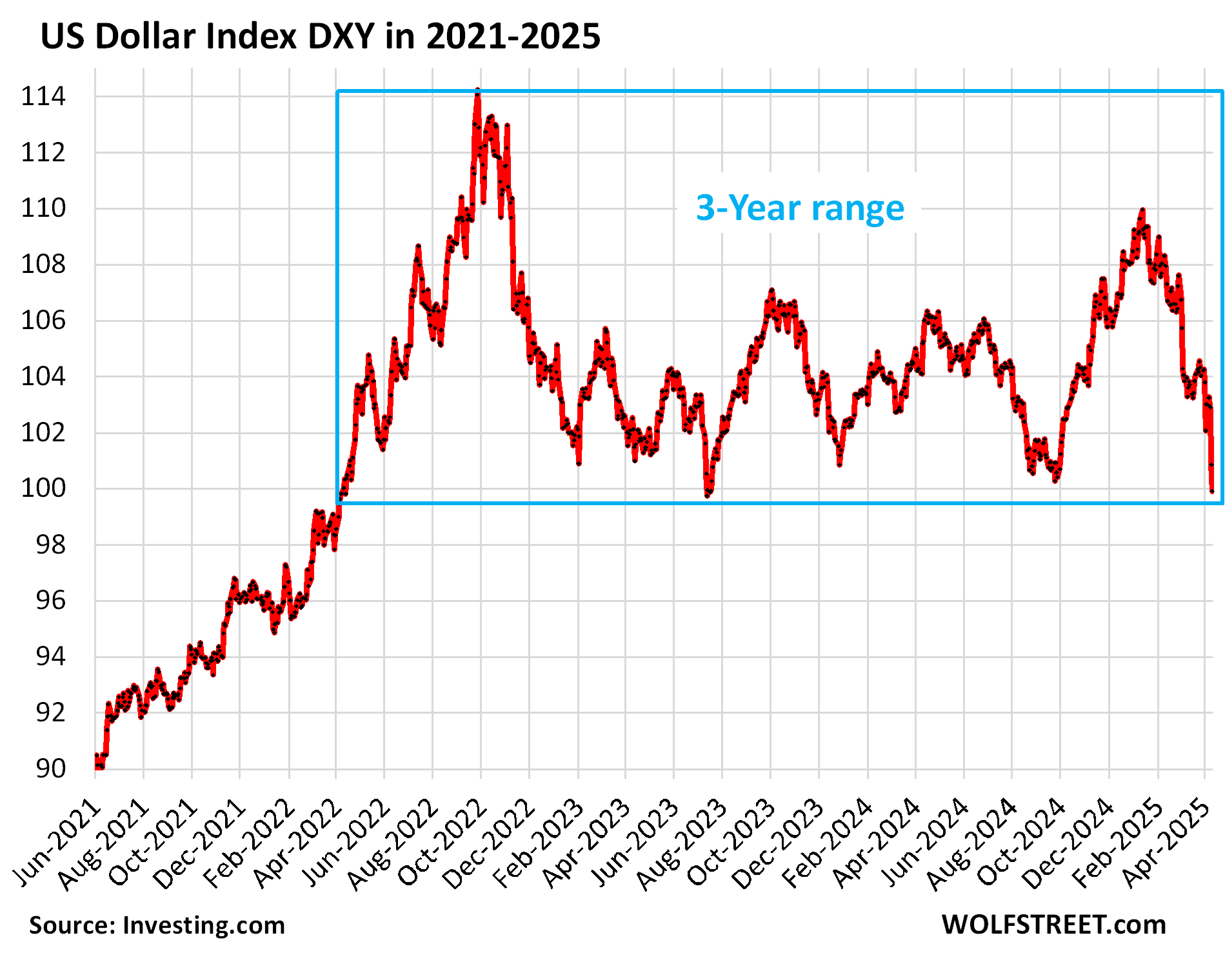

The dollar bash-down.

The White-House bash-down of the dollar was also very effective, but unlike the 10-year Treasury yield, the dollar hasn’t snapped back yet. Though it will sooner or later.

The dollar remains in its 3-year trading range and is higher than it was before that trading range. I had a little bit of fun on Friday with the catastrophist handwringing in the media over the dollar: OMG the Dollar Is Collapsing, or Whatever.

The dollar index [DXY], representing a basket of six currencies dominated by the euro and yen, dropped from 110 in January to 99.78 on Friday. But that drop was a lot smaller than the drop in 2022, and a lot smaller than prior drops, after which the dollar always bounced back. There were many years when the DXY was below 80. And at the current level, the dollar is still relatively high compared to where it had been in the prior 50 years. My article also includes a chart going back to the 1970s.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post 10-Year Treasury Yield Snaps Back to February’s 4.5%, Yield Curve Re-Un-Inverts, Mortgage Rates Back at 7% appeared first on Energy News Beat.

“}]]

Energy News Beat